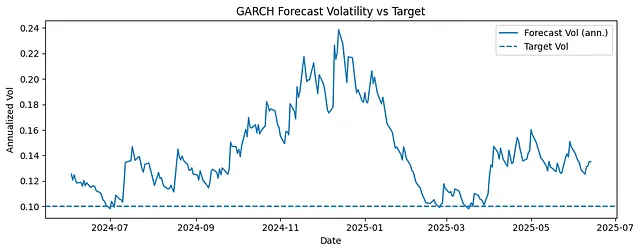

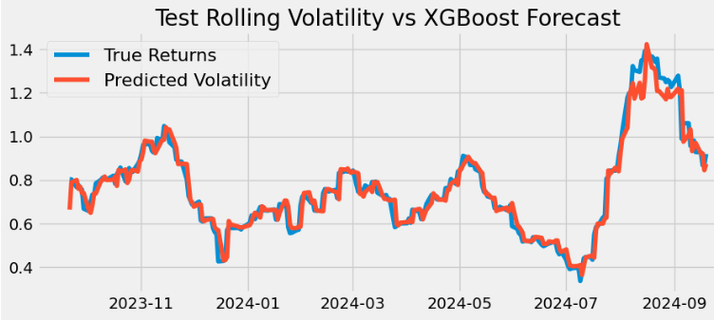

GARCH Volatility Modeling with Python: Risk-Adjusted Position Sizing

Use tomorrow’s volatility estimate to size today’s position—so risk stays stable when markets do not.

This post shows how to forecast volatility with GARCH, convert it into a position multiplier, and sanity-check the result with standardized residuals and simple diagnostics in Python.