72/ Finally had some time to continue and this chapter might take a while, and I might need to read it several times. Funnily it seems that she agrees that the dollar is special. I learned a thing, though, after the world abandoned the gold standard we kind of didn’t, we pegged the dollar to gold and a lot of the other currencies to the dollar. This was called the “Bretton Woods system”.

https://en.wikipedia.org/wiki/Bretton_Woods_system

73/ Well there it is, I wasn’t off base after all. Because of the position of the dollar the Feds actions, aimed at the domestic economy, has a much larger international blast radius.

74/ Some Norwegians have recommended that we peg the NOK to the Euro, and I think that our feeling that Denmark is similar to us culturally distracts us from recognizing how fundamentally different our economies are. Most importantly the petroleum “enhanced” economy of Norway and the fact that Denmark is a member of the EU and we are not, even with our extensive trade agreement.

75/ Chapter 5: “‘Winning’ at trade” is interesting, but doesn’t really go into the depth I’d like (but I guess after reading 4 Econ books in a row I’m not the target readership). The chapter is very “political” and idealistic rather than descriptive, but that was a tendency we saw earlier too. The basic idea is that a trade deficit isn’t a bad thing. She goes on to envisage a world economy that is more… equitable? It argues for developing countries to focus more inward, and diversifying their economies, perhaps making them less vulnerable to the global markets. It argues against losing control over one’s own currency (its MMT, so obviously). It makes clear that the dollar gives the US an outsized influence and leverage over the rest of the world.

She criticizes both democrats and republicans, but seems to have a soft spot for Bernie Sanders. He hired her to work at the Capitol, so I guess that makes sense.

The MMT premise seems to be that you don’t have to “have the money” to fund guaranteed full employment or “entitlement programs”, because the control over the currency means that the government always “has the money” to pay.

76/ The “winning vs losing” at trade is explicitly directed at Donald Trump. But she spends a lot of time emphasizing that American workers have lost jobs (“well paid union jobs” comes up several times) when production moved offshore.

It feels to me like she is arguing for a midpoint, a more protectionist approach, but not measuring in trade deficit/surplus, but instead in… standard of living?

She gets slightly into the topics of “The Shock Doctrine” in that the international trade organizations and the world bank became dominated by extremist (my word) capitalist forces.

77/ What I appreciate:

1. She is clear that the challenges that face us in the years to come are global, and that we have to work together to solve them, as partners instead of competitors.

2. She is not proposing some sort of bloody global revolution.

3. She is slowly selling me on the idea that guaranteed employment, benefits and entitlement programs are a safeguard against radicalization. I have mostly thought of these things as the “right thing to do” rather than a way to maintain peace.

4. The ideology is inclusive instead of divisive, and therefore doesn’t rest on the boogeyman approach of both the fundamentalist left and right. She doesn’t use immigrants or poorly veiled antisemitic tropes (the evil rich man of various formats) to paint some other group as the enemy.

1. She is clear that the challenges that face us in the years to come are global, and that we have to work together to solve them, as partners instead of competitors.

2. She is not proposing some sort of bloody global revolution.

3. She is slowly selling me on the idea that guaranteed employment, benefits and entitlement programs are a safeguard against radicalization. I have mostly thought of these things as the “right thing to do” rather than a way to maintain peace.

4. The ideology is inclusive instead of divisive, and therefore doesn’t rest on the boogeyman approach of both the fundamentalist left and right. She doesn’t use immigrants or poorly veiled antisemitic tropes (the evil rich man of various formats) to paint some other group as the enemy.

78/ I think 4 is essential for progress to be made, because the current right and left political movements are focusing on targeting hate and animosity towards another group of humans, rather than at an inequitable system. And that only perpetuates that system because that energy is wasted on being unproductive (and hateful, which sucks the soul out of everyone at a time when we need a surplus of generosity, in my view)

79/ But the book is supposed to not just be a work of ideology, but provide a way through this mess we’re in, in the aftermath 🤞of a global economy dominated by extremist capitalism.

And that premise is based on this currency “trick”, and there I am not yet convinced tbh.

80/ Chapter 6 is on entitlement programs, but I think I’m going to go back to chapter 4, which I skipped, hoping that might be a bit more illuminating on the MMT side.

81/ why are we humans so ready to blame all of our problems on “the other”. With all that we know about the consequences of this, we seem to fall for it every time. Why do we let them make us fight each other in some grotesque gladiator game? Is it our need for simple solutions? Do we need someone to hate?

That train of thought reminded me of this Norwegian song

https://youtu.be/9QxGKTTtYgM?si=G9in1FTPPu2q49_a

That train of thought reminded me of this Norwegian song

https://youtu.be/9QxGKTTtYgM?si=G9in1FTPPu2q49_a

Noen å hate

82/ Norwegian lyrics:

“Han der er ikke sånn som deg

Fort deg bort og ta han

Det er like godt som sex

Å banke en stakkars faen

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Hør lyden av nakker som knekker

Hør lyden av kjøtt som sprekker

Det er bare å følge fingeren som peker

Dit hvor de voksne leker

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Han der er ikke sånn som deg

Fort deg bort og ta han

Det er like godt som sex

Å banke gørra ut av en stakkars faen

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?”

“Han der er ikke sånn som deg

Fort deg bort og ta han

Det er like godt som sex

Å banke en stakkars faen

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Hør lyden av nakker som knekker

Hør lyden av kjøtt som sprekker

Det er bare å følge fingeren som peker

Dit hvor de voksne leker

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Han der er ikke sånn som deg

Fort deg bort og ta han

Det er like godt som sex

Å banke gørra ut av en stakkars faen

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?”

83/ Rudimentary English translation:

“He's not like you

Hurry over and get him

It's as good as sex

To beat a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Hear the sound of necks snapping

Hear the sound of meat cracking

You just have to follow the pointing finger

Where the adults play

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

He's not like you

Hurry over and take him

It's as good as sex

Beating the crap out of a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?”

“He's not like you

Hurry over and get him

It's as good as sex

To beat a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Hear the sound of necks snapping

Hear the sound of meat cracking

You just have to follow the pointing finger

Where the adults play

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

He's not like you

Hurry over and take him

It's as good as sex

Beating the crap out of a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?”

84/ Ok, chapter 4 “Their red ink, is our black ink”. I think it was Keen in one of his podcast episodes who said something that I hadn’t considered. From memory: as a country’s economy grows, whatever that means, the money supply would need to grow too.

Looking at population growth alone that makes sense to me. And that means that my mental model of a fixed “amount of money we have” isn’t correct. It would, at least over longer periods of time, need to be elastic in some way. And I can’t see how that could be a global zero sum game either, since many countries that were poor a century ago, and are still poor today, often still have a “bigger” economy than they did a century earlier.

85/ So if “the amount of money” we have is flexible, and that the value of a currency is affected by similar forces as stocks and gold and whatever… that seems to support that money is “artificial”. And of course, economists would say “of course it is, we abandoned the gold standard ages ago”, but to me that hasn’t been obvious, because even if we don’t peg our currency to something tangible (directly or indirectly) that doesn’t mean that we can consciously “grow money” on a money tree.

86/ I can accept that the relationship with a currency is different when one has control of it, rather than being just a user of it. But it is nonobvious to me (still) that manipulating the money supply can be done largely with impunity. My brain (perhaps polluted by economics) feels that having more of something would make it less valuable. But maybe that’s not a universal law… maybe Maslow should have a say. If we take a consumable, perishable product that is a necessity through being food. Would having a lot of bread make it worthless? We still pay for bread, even when stores and bakeries throw away bread every day. So… maybe (bombshell 😂) the economic theory here is too simplistic? Maybe money doesn’t work the way we have been taught that it does?

87/ It’s funny because in my paper on Costa Rica (which I mentioned in another thread) one of the things that I argued was that what people believe (even if it is not currently true) is a driver for it to become true. So if a country started to print money at will, even if it might not matter (possibly 🤷🏻♀️) currency traders might believe that it does, and by the nature of their role, they might make it so it does matter, by weakening the currency through exchange rates.

88/ And as I mentioned earlier, maybe the dollar has some protection here. That through being a global “gold equivalent” everyone has a stake in it not tanking, even, I would guess, individual currency traders.

89/ Well, shit this is damning 😂

“Cases 5 and 6 underscore the lack of a causal relationship between rapid M2 growth [growth in money supply] and high inflation, because when we increase the threshold of nominal M2 growth to from 60 percent in five years to 200 percent in five years, it is followed by high inflation even less frequently than in Cases 3 and 4. This is, of course, the opposite of what one would expect if high M2 growth causes high inflation.”

(h/t @igimenezblb) https://www.ineteconomics.org/perspectives/blog/rapid-money-supply-growth-does-not-cause-inflation

“Cases 5 and 6 underscore the lack of a causal relationship between rapid M2 growth [growth in money supply] and high inflation, because when we increase the threshold of nominal M2 growth to from 60 percent in five years to 200 percent in five years, it is followed by high inflation even less frequently than in Cases 3 and 4. This is, of course, the opposite of what one would expect if high M2 growth causes high inflation.”

(h/t @igimenezblb) https://www.ineteconomics.org/perspectives/blog/rapid-money-supply-growth-does-not-cause-inflation

90/ I know after the rant I’ve been on the last few weeks that I shouldn’t be surprised that they just inferred from their damn models, with zero data to back it up… but shit I still am. Need to figure out if there has been discussions around this result.

91/ Oh here he goes into another side of this (very US centric): that the increase in household wealth as a result of deficits tends to be tied to real estate and stock values, and that results in wealth distribution inequality, because most poor people don’t own homes nor stocks.

https://youtu.be/wuonrlKefRM?si=7TUvGs-JeUI2AWW5

https://youtu.be/wuonrlKefRM?si=7TUvGs-JeUI2AWW5

The Paradox of Debt | Richard Vague | TEDxCapeMay

92/ As some folks have alluded at (where does the new money actually go) and based on something she says earlier in the book (that deficits have actually been too low) I started wondering. Imagine I have a truck full of dirt and I tell you I’m going to pour it out, you’d think it would create a pile of dirt, right? But what if I pour it into a hole. We don’t get a pile, we lose a hole…

The thing that I think MMT are arguing is that “debt” isn’t “debt” if it’s monopoly money you made up. To you as the money machine it behaves differently. And debt isn’t debt. It’s potentially pothole filling. But that means something is absorbing money, and don’t just say “rich people” because that is lazy. Are there holes? Where are they? What would be the effect of filling them? I’m assuming that filling different holes would have different effects. And maybe that’s MMTs thing: to fill the unemployment/underemployment hole? And from there achieve an effect?

93/ Even if we accept that money doesn’t work the way it works for us “money users”, for the “money creators”… and tbh that study was pretty darn convincing, I thought (I’d love to see an opposing view). Then… that doesn’t actually prove (in my mind) that all kinds of “holes” in the economy would behave the same when “filled”. Just because there isn’t a causal relationship between printing money and inflation, do we know what printing money actually does? And does it matter who gets it?

94/ Still in chapter 4. She was discussing another economist, Wynne Godley, and so I had to look him up and that opened another line on economic models: equilibrium models (the “mainstream economics” models) and a set of models referred to as “accounting models”.

Steve Keen, who a lot of folks have brought up (the guy with the podcast “Debunking Economics”) seems to be one of the people who are proponents of “accounting models”.

And it seems to me that MMT draws from the work of economists in this area.

Wynne Godley was credited for predicting the financial crisis based on his model.

This paper looks very interesting because it seems to contrast the two approaches. Which tends to be illuminating in my experience.

“No one saw this coming. Understanding financial crisis through accounting models”.

https://pure.rug.nl/ws/portalfiles/portal/2646456/09002_Bezemer.pdf

95/ so far my (quite shallow) understanding is that these “accounting models” model flows of money. With the basic premise that money has to come from somewhere and go somewhere. Or more accounting-wise that a subtraction one place has to lead to an addition of equal size (possibly the sum of multiple additions) somewhere else.

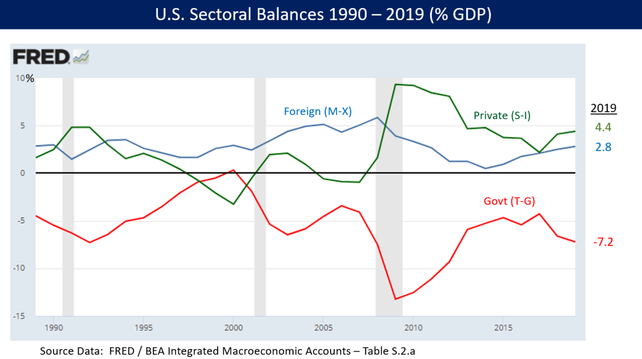

This relates to the idea that MMT presents, which Wynne Godley also seems to have supported and Richard Vague (above article and TED talk), that a deficit for the state necessitates a surplus somewhere else. Found this graph from Godley using his “sectoral financial balances” framework, depicting the US economy. This graph is very similar (perhaps identical?) to what Vague shows in his TED talk. They both show what seems to be an inverse relationship between a public deficit and a private surplus.

96/ I am worried that I’m finding this theory appealing just because the others are so terrible and so I’ve been primed to be positive to this one.

Which funnily enough is called “Anchoring effect” and features prominently in “behavioral economics”

https://en.wikipedia.org/wiki/Anchoring_effect

Which funnily enough is called “Anchoring effect” and features prominently in “behavioral economics”

https://en.wikipedia.org/wiki/Anchoring_effect

97/ Brains suck

98/ Ok, but if this is true, this seems to imply to me that austerity is counterproductive? That it would push an economy further into recession? Am I reading this wrong?

99/ my logic being that austerity means in effect a savings on the public side which would (in an accounting model) require “sucking” that money from other places in the economy, and that seems to mean mainly private sector. So to achieve plus on the public side using this mechanism would require minus on the private side.

100/ but hold up… I just argued that the size of the money supply was not fixed… but I guess that fits… because the public side can create money to cover it’s deficit, but private sector doesn’t have that option. So under austerity we create a zero sum game.

Am I even making sense anymore ?

101/ I’m sorry, but I have a lifetime of indoctrination to overcome here, and magic no consequences money tree seems a bit far fetched tbqh

102/ Ooh a rant against MMT by a Keynesian economist 🤓

https://www.nytimes.com/2019/02/25/opinion/running-on-mmt-wonkish.html

https://www.nytimes.com/2019/02/25/opinion/running-on-mmt-wonkish.html

103/ seems to me from reading this and some of the references that the disagreement seems to be “technical”. Krugman seems to agree that the fear of deficits is overblown, but seems to argue that interest rates are another tool to manage possible inflation. Tbh I haven’t gotten the opposite impression yet from the book, but maybe I missed it.

One thing I do wonder about is that if the deficit is in the form of bonds, won’t higher interest rates affect the cost of the accumulated deficit? Wouldn’t the public side now also have to pay more for the accumulated deficit? How does that work?

Maybe I don’t know how any of this works

104/ Also why reach immediately for interest rates? Is it because tax hikes are politically harder to pass? Interest rates seem to bring with them unintended consequences like increased profits for private sector banks and things like rent increases. In an inflationary economy I would think that the poor aren’t those “heating” things up.

105/ she is describing a model for interest rate that I think she is going to argue against. In it there seems to be a mechanism where one imagines that the private sector and public sector compete for loans in the same fixed sized market. And so the public sector deficits are in this model financed by loans in this market. And therefore the increased deficit would then be a significant increase in demand on a finite supply of money. And therefore drive the interest rate up.

But… that’s not how it works? In the real world? The banks increased their interest rates when the central bank did. So this model doesn’t make sense at all to me.

106/ Halfway through this but tbh this is a much more convincing argument for this phenomena than the pretentious colonial-envy drivel by Piketty. Young people are struggling because they are poorer than previous generations.

https://youtu.be/ZuXzvjBYW8A?si=g_1Z9XfgsTpioq2G

(h/t @Di4na)

https://youtu.be/ZuXzvjBYW8A?si=g_1Z9XfgsTpioq2G

(h/t @Di4na)

Have the Boomers Pinched Their Children’s Futures? - with Lord David Willetts

107/ I wonder if the distribution he is presenting is the same in other countries. Because according to him, boomers are consuming more than young people right now. And they are doing that from inside of their unmortgaged homes. Meanwhile young people get berated for being poor and are required to reduce their carbon footprint to a fraction (1/7?) of the boomers. Jeez.

108/ omg these numbers are mind blowing. Boomers are absolutely killing it. And young people are so screwed.

109/ Related/unrelated : Piketty pisses me off even more now. Because instead of just presenting the facts, I had to accompany him on his colonialist reminiscence tour. For data that is absolutely meaningless. Interspersed with the only woman he knows the name of, Jane Austen.

110/ if y’all are new here, you can experience my spiraling rage at Piketty’s Capital in that books thread (also linked to in my pinned thread of book threads)

https://social.vivaldi.net/@Patricia/112704863073553929

https://social.vivaldi.net/@Patricia/112704863073553929

Patricia Aas (@[email protected])

4/ “Capital in the Twenty-First Century” by Thomas Piketty https://social.vivaldi.net/@Patricia/112681938811222913

111/ oh my, I had forgotten how complete the Piketty-roasting Past Patricia did was 🧨🔥 good for her.

112/ Getting towards the end of chapter 4 (which I skipped earlier) and she’s talking about the crisis with Greece. And I have a question for EU folks: From a lot of these books I have gotten the impression, though maybe they haven’t gone out and said it, that Germany and perhaps France has an outsized influence/control over the Euro monetary policy. Is that accurate?

@Patricia There certainly are reasons to believe so. Schäuble seemed to essentially set the post-2008 policy. It's also indicative that while procedures against countries for failing to fulfil the stability criteria (debt, deficit...) were initiated against Greece, Portugal, Italy, etc, France and Germany violated stability criteria before 2008 without this happening to them.

https://www.theguardian.com/business/2003/nov/25/theeuro.politics

And there's still similar asymmetries going on: https://www.bruegel.org/analysis/fixing-germanys-fixes-european-commissions-fiscal-governance-proposal

@Patricia Absolutely. Most of Greece's creditors were German banks, and in general a lot of the financing comes from German investment. France used to have more direct impact, it's slowly fallen behind Germany. I recommend watching the documentary "In The Eye of the Storm" to get an idea of what economic negotiations within the Eurogroup looks like, especially from the perspective of what is perceived as a lesser country like Greece. The first half focuses on Yanis Varoufakis becoming the Greek finance minister during the negotiations of the debt crisis, and the second half on his more recent political struggles. He's one of the few economists I listen to, especially because he explicitly says that it is not a science.

https://vimeo.com/ondemand/eyeofthestormenglish

https://vimeo.com/ondemand/eyeofthestormenglish

In The Eye Of The Storm — The Political Odyssey Of Yanis Varoufakis

@Patricia Definitely yes. At least this is my perception from one of the southern countries (Spain)

113/ This speech is very interesting and recent. Only a couple of weeks old. And also here the speaker, Philip R. Lane, member of the Executive Board of the ECB, seems to say that the relationship between growth of the money supply and inflation is not as clear as one used to think. This is very interesting… I think I need to read it more carefully.

https://www.ecb.europa.eu/press/key/date/2024/html/ecb.sp240626~0cdeaedbb1.en.html

https://www.ecb.europa.eu/press/key/date/2024/html/ecb.sp240626~0cdeaedbb1.en.html

114/ And here from the Congressional Research Service

Deficit Financing, the Debt,

and “Modern Monetary Theory”

https://sgp.fas.org/crs/misc/R45976.pdf

115/ I have read a lot from the aftermath of the financial crisis. And a lot of mainstream economists are all “Listen, inflation is too low, interest rates are also low and employment is high… and according to our models that isn’t possible.” And then they stop there. Can you imagine an actual scientific field that again and again had actual proof their models are wrong yet absolutely zero impulse to go: “ok, looks like this is all bullshit, maybe we should try to figure out how the system/economy actually works”

@Patricia Reading much of this thread, I finally remembered that I read "History of Greed" (by David E. Y. Sarna) some years ago. It isn't as much about economy as such, but examples of how markets of various kinds have been exploited since the early tulip days of Holland until the Bernie Madoff scandal. (and looking it up, turns out my description above is pretty much the sub--title of the book ...)

@Patricia Also, on the topic the financial crisis (I guess you may very well know this), The Black Swan by Nassim Taleb is more or less considered to have predicted the financial crisis of 2008. (Anecdote: I remember being in Seattle the late summer of 2007, seeing some slight worry at those sub-prime loans on the front pages of the local newspapers).

@larsivi it’s funny because my family and I did a road trip the summer of 2007, we drove from New York to the Florida Keys, and all the way we would hear commercials on the radio saying: “No Credit? Bad Credit? No Problem! We can get you a loan today!”

For us as Norwegians it was mildly absurd, but I guess we just assumed it was “an American thing”.

For us as Norwegians it was mildly absurd, but I guess we just assumed it was “an American thing”.

@larsivi I never did read the Black Swan. I always thought it was a business book

@Patricia I had it recommended to me by someone, and I'm pretty sure that person wouldn't have recommended a business book :) The book is more mathematical, on probabilities and how (very) unlikely, but high impact, events are handled in risk evaluations.

@larsivi as far as I understand it isn’t very technical, it was a New York Times bestseller, as far as I have gathered a “pop” business book

@larsivi but I guess it’s one of those books I have to read because I’ll know what people are saying, but where I almost always conclude that it could’ve (and should’ve) been a blog post

@Patricia I don't entirely remember, but it could have been a book I listened to rather than read. In any case, I liked it a lot back then, and doubt that I would if it was too long (although the points of it could of course almost certainly be condensed).

116/ But one thing I haven’t read much about is this inflation they’re currently fighting with interest rates globally. What do they think caused that? The EU guy didn’t seem to think it had anything to do with the financial measures during the pandemic, but rather fallout from the supply chain breakdown? I really need to read that speech more closely.

For Norway imo imported inflation of 2-3 percent doesn’t really matter when exchange rates mean that imports are 25(?) % higher than a couple of years ago. And I’ve realized that people aren’t distinguishing the two much in the media. But the interest rate hike that they are apparently doing to fight the insignificant inflation is killing households who are struggling with food prices due to the weak NOK.

For real. I don’t get the interest rate hike at all, it seems purely destructive for no reason. It clearly has zero effect on the value of the NOK.

117/ For real, how does this make any sense? Companies costs are increasing because the NOK is historically weak and interest rates shot up, so costs are way up and demand is way down. So their answer is to continue to beat Norwegian households into “submission” because they are already lying on the ground?

“There is uncertainty about the further development of the Norwegian economy. If companies' costs continue to rise rapidly or the krone becomes weaker than forecast, price inflation may remain high for longer than we currently envision. Then the committee is prepared to raise the interest rate again.” (Google translation)

https://www.norges-bank.no/kort-forklart/inflasjon/

@Patricia

I am no economist, but I think one idea is that higher interest rates ought to help with the weak NOK by increasing demand.

A higher interest rate means that just holding NOK in the bank gains more interest, and so it is more attractive for investors to buy NOK.

Of course, this is just an armchair view of how people ought to behave, which seems to be how economics works 🤷♂️

I am no economist, but I think one idea is that higher interest rates ought to help with the weak NOK by increasing demand.

A higher interest rate means that just holding NOK in the bank gains more interest, and so it is more attractive for investors to buy NOK.

Of course, this is just an armchair view of how people ought to behave, which seems to be how economics works 🤷♂️

@audunska it’s an experiment, but it’s not working, all countries are raising their interest rates to fight the global 2-3% inflation. And the inflation isn’t because the Norwegian domestic economy is “overheated”. Granted export companies are raking it in on the weak NOK, but for them the interest rate is insignificant. But the interest rate is impacting everyone and comes on top of price hikes because of inflation and weak NOK. So we’re just punishing those who are already hurting with zero results to show for it. And zero ways they can improve the situation.

@Patricia yes, but in addition to the narrative about the overheated economy, there's the idea that a high interest rate drives up demand for the NOK, and thus combats the weak exchange rate.

But anyway, investors seem to shy away from the NOK whatever the interest rate, so I'm not claiming it works.

But anyway, investors seem to shy away from the NOK whatever the interest rate, so I'm not claiming it works.

@audunska and they can get the same interest rate in pretty much any country right now without the currency risk. It doesn’t make sense.

@Patricia one could argue that if the interest rate was significantly lower than other currencies, Norwegian money would escape to those other currencies, lowering demand for the NOK and tanking the exchange rate further...

@audunska why would you take a 20% currency hit for a 2% interest rate increase? That doesn’t make sense to me

@Patricia One story I find convincing: Trigger was a supply chain shock because of COVID (per e.g. Paul Krugman or Claudia Sahm), hence world wide inflation.

Then other factors prolonged it, like Ukraine war.

Also: corporations feeling confident consumers will pay more.

Pretty sure I very much butchered that last argument but the Odd Lots podcast episodes with Isabelle Weber were great about that

@Patricia This is the 2nd one I believe: https://www.bloomberg.com/news/audio/2023-06-07/isabella-weber-on-the-big-rethink-of-inflation-podcast

[]

Earlier this year, Odd Lots talked about the idea of companies taking advantage of bottlenecks and other disruptions to raise their prices. Since then, the notion of this type of corporate-led inflation has burst into the public discourse with central bankers and politicians all taking a closer look. But how does this type of inflation differ from more traditional economic interpretations of prices, and what are the implications for monetary and economic policy? In this episode, we talk once again to Isabella Weber, the University of Massachusetts Amherst economics professor who dubbed this phenomenon "sellers' inflation" in a paper published earlier this year. She talks about how the way we think about inflation is changing and her own experience of seeing public attitudes shift in real time.

@trost thanks!

@trost “We should recognize the recourse to higher interest rates for what it is: a strategy to dump the costs of inflation on to labor (by suppressing wages), on to social programs (through austerity), and on to future generations (by discouraging investment).”

https://www.project-syndicate.org/commentary/sellers-inflation-diagnosis-accepted-but-old-interest-rate-policies-remain-by-isabella-m-weber-2023-07

https://www.project-syndicate.org/commentary/sellers-inflation-diagnosis-accepted-but-old-interest-rate-policies-remain-by-isabella-m-weber-2023-07

118/ This, however, makes more sense to me.

https://youtu.be/fjoDjv1R3to?si=0jJNF-sEFAdFC8rR

https://youtu.be/fjoDjv1R3to?si=0jJNF-sEFAdFC8rR

Sellers Inflation [Isabella Weber]

119/ Ok, I’m not alone with this feeling. One could’ve taxed corporations that are apparently creating this inflation, but instead we’re going make regular people poorer and/or unemployed. The same people who are struggling with the inflation in the first place. Sounds very Friedman’esque

https://youtu.be/RyIeC21XeLs?si=O7YOGfZd_ETpc8vR

https://youtu.be/RyIeC21XeLs?si=O7YOGfZd_ETpc8vR

Jon Stewart Forces Economist To Admit Capitalism Screws Us All

@Patricia actually... The term of "inflation" itself is... Problematic.

Inflation of *what*. Typically car price, especially second hand, and housing cost have shot up significantly. Noone knows exactly why but I have some ideas.

The other elements of CPI are usually down or stable.

So looking at it as a single "inflation" term is... Dangerous.

@Patricia and once again... What is corporate profit ? Who get the money ?

@Di4na unsurprisingly I haven’t seen a single number from any economist yet, but they are all to happy to label it

@Patricia ikr. You get these labels and then poof. No need to look into the box.

@Patricia for a look into the complexity of inflation, this is a good start.

Once again, not an endorsement of everything, just another brush of paint on the canvas

https://economicsfromthetopdown.com/2021/11/24/the-truth-about-inflation/

@Patricia my personal take at inflation is simpler.

People are retiring, which is heavily unbalancing the flow of money, wealth, salaries and demands.

The vast majority of Western economy is moving to support wealthy (comparatively, in average) Boomers pensioners. That means a lot of bad pay job (home mobility and nursing) that are highly dangerous, from a generation of renters (landlord being boomers) who work for corps which profit pay the pensions.

What we are seeing is the impact of that

120/ Chapter 7. “The Deficits That Matter” Is pretty damning tbh, it seems to be mostly about how the US has fallen desperately behind other comparable countries. On all types of metrics, from child mortality to life expectancy.

121/ Finished chapter 7 and 8 and it is pretty clear to me that this is mainly aimed at the US, and seems to be intended as an economic lever to shift the US in a more social democratic direction.

This is her summary of MMT

122/ and tbh I think such a move would be positive thing not only for the US population, but also for the whole planet.

123/ I have been trying to find someone saying what is causing this inflation. And it's weird how little there is to find on this. But I found a page on the national statistical institute of Norway (SSB) talking about inflation in 2023. And it is really funny how they even point out the same feedback loops I've talked about in this thread (plus some more):

- rents are up (increased interest rates are probably a factor)

- imported goods are up (weak NOK is probably a factor)

Other things they brought up was that energy prices had been very high and that those losses were probably also being priced in.

The thing is... That means that we are turning up interest rates partially because we turned up interest rates and partially because our currency is weak and that energy prices were high a year ago. And turning up interest rates is not made to fix any of that.

It is made to cool down an overheated (too much money, too much spending) economy.

But that isn't what the economy looks like. But since they have reduced the entire state of the economy into one number (plus some including this, excluding that numbers), all context is gone and they pull out the same hammer that is part of the reason we got in this mess.

https://www.ssb.no/priser-og-prisindekser/konsumpriser/statistikk/konsumprisindeksen/artikler/kraftig-prisvekst-i-2023

Kraftig prisvekst i 2023

Året vi har lagt bak oss var nok et spesielt år når det gjelder prisvekst. I et historisk perspektiv steg prisene uvanlig mye. I motsetning til året før, da prisveksten økte kraftig for de fleste varer og tjenester som husholdningene kjøper, var bildet litt mer sammensatt i 2023.

124/ Their whole model is based on the assumption that when prices go up it is because demand is up. But sometimes prices go up because costs are up. And... that is not fucking supported.

I don't know what to say.

@Patricia Maybe it's what you're alluding to, but the big case of inflation without demand increase was '70s stagflation from the oil shock.

Conventional wisdom is that this was brought under control by high interest rates, despite the economy being weak (very painful). I'm sure you can find more subtle takes.

The lesson about avoiding stagflation is to maintain military supremacy over oil producers. ;)

@sgf and yes, that would be very interesting to read more about

@pvaneynd @Patricia Sorry, I don't have anything non-economist on it. My knowledge comes from reading undergrad economics texts.

I took a look at Wikipedia, https://en.wikipedia.org/wiki/Stagflation#Responses covers the "escape through high interest rate" part of it, but the whole page makes it sound like "it's complicated" - for example, the trigger being more than oil prices, and many, many different models competing to explain it.

Inflation, being partly based on expectations, is very "complex adaptive systems".

125/ Ok, this is fascinating. Norway has one of the largest sovereign wealth funds in the world, right? We’re loaded as a country. But I just read that Norway has debt, which… what? Why? So I had to look it up and unfortunately this Wikipedia page is only in Norwegian. But to me it describes parts of what MMT talks about. That state “debt” isn’t really debt, but largely a technical mechanism to control the money supply. It makes bonds available to buy and buys them back depending on if it wants to grow or shrink the money supply. Am I off base here?

https://no.wikipedia.org/wiki/Norges_statsgjeld

https://no.wikipedia.org/wiki/Norges_statsgjeld

@Patricia That's fairly close to my understanding.

There's more about that here: https://www.norges-bank.no/en/topics/Government-debt/

@Patricia yep thats my (not an economist) understanding of how many governments use debt

@Patricia Makes it all the more stupidly funny that Germans think that government debt is the same as household debt.

@alper the problem there might be the euro. If the European Central Bank doesn’t manipulate the currency in a way that is optimal for all members then individual countries don’t have the necessary flexibility

@Patricia during the mining boom, when Australia was running consistent surpluses and had negative net debt (ie: was owed more than it was owing), the government continued to issue bonds because various parts of the financial system absolutely require owning government debt. https://en.wikipedia.org/wiki/Australian_government_debt

@Patricia yep that is more or less what i means. Note also that "good debt" (like government one for a stable rich government) is kinda the basis of the whole banking and investment system. It needs to exist, otherwise it is hard to invest. Another kind of "good debt" is usually land ownership that can be transformed into stable income, like with "commodity" grain. That is why the US produce so much corn, even if it is cheap and bad one.

126/ Jon Stewart on MMT with Stephanie Kelton

https://youtu.be/0G6obeUKWmw?si=-rW1dPklrdytZCMz

https://youtu.be/0G6obeUKWmw?si=-rW1dPklrdytZCMz

How Do We Fix The Economy? Modern Monetary Theory, Explained | The Problem With Jon Stewart Podcast

127/ so back to my radiator system mental model. Question that seems partially answered by the above (which completely breaks with Friedmans model btw) is that the massive accumulation of wealth, on the part of the already wealthy, doesn’t cause inflation precisely because they don’t spend it. So that would, in the radiator system metaphor, mean that you keep on filling water into the system but some of the occupants in the building are tapping out water to fill their indoor swimming pools, or something. The system doesn’t come under massive pressure because of the excess water/money because it is being siphoned out continuously.

@Patricia i just keep being reminded of this segment from the Hitchhiker's Guide to the Galaxy https://youtu.be/PQjgMF_20dE?t=190

Galactic Tax Hole | The Hitchhiker's Guide to the Galaxy | BBC Studios

@mrsbeanbag “Spending a year dead for tax reasons” 🤣