“Cases 5 and 6 underscore the lack of a causal relationship between rapid M2 growth [growth in money supply] and high inflation, because when we increase the threshold of nominal M2 growth to from 60 percent in five years to 200 percent in five years, it is followed by high inflation even less frequently than in Cases 3 and 4. This is, of course, the opposite of what one would expect if high M2 growth causes high inflation.”

(h/t @igimenezblb) https://www.ineteconomics.org/perspectives/blog/rapid-money-supply-growth-does-not-cause-inflation

https://youtu.be/wuonrlKefRM?si=7TUvGs-JeUI2AWW5

The Paradox of Debt | Richard Vague | TEDxCapeMay

92/ As some folks have alluded at (where does the new money actually go) and based on something she says earlier in the book (that deficits have actually been too low) I started wondering. Imagine I have a truck full of dirt and I tell you I’m going to pour it out, you’d think it would create a pile of dirt, right? But what if I pour it into a hole. We don’t get a pile, we lose a hole…

The thing that I think MMT are arguing is that “debt” isn’t “debt” if it’s monopoly money you made up. To you as the money machine it behaves differently. And debt isn’t debt. It’s potentially pothole filling. But that means something is absorbing money, and don’t just say “rich people” because that is lazy. Are there holes? Where are they? What would be the effect of filling them? I’m assuming that filling different holes would have different effects. And maybe that’s MMTs thing: to fill the unemployment/underemployment hole? And from there achieve an effect?

94/ Still in chapter 4. She was discussing another economist, Wynne Godley, and so I had to look him up and that opened another line on economic models: equilibrium models (the “mainstream economics” models) and a set of models referred to as “accounting models”.

Steve Keen, who a lot of folks have brought up (the guy with the podcast “Debunking Economics”) seems to be one of the people who are proponents of “accounting models”.

And it seems to me that MMT draws from the work of economists in this area.

Wynne Godley was credited for predicting the financial crisis based on his model.

This paper looks very interesting because it seems to contrast the two approaches. Which tends to be illuminating in my experience.

“No one saw this coming. Understanding financial crisis through accounting models”.

https://pure.rug.nl/ws/portalfiles/portal/2646456/09002_Bezemer.pdf

95/ so far my (quite shallow) understanding is that these “accounting models” model flows of money. With the basic premise that money has to come from somewhere and go somewhere. Or more accounting-wise that a subtraction one place has to lead to an addition of equal size (possibly the sum of multiple additions) somewhere else.

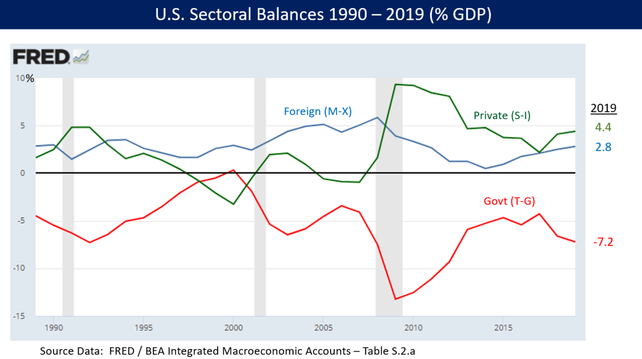

This relates to the idea that MMT presents, which Wynne Godley also seems to have supported and Richard Vague (above article and TED talk), that a deficit for the state necessitates a surplus somewhere else. Found this graph from Godley using his “sectoral financial balances” framework, depicting the US economy. This graph is very similar (perhaps identical?) to what Vague shows in his TED talk. They both show what seems to be an inverse relationship between a public deficit and a private surplus.

Which funnily enough is called “Anchoring effect” and features prominently in “behavioral economics”

https://en.wikipedia.org/wiki/Anchoring_effect

100/ but hold up… I just argued that the size of the money supply was not fixed… but I guess that fits… because the public side can create money to cover it’s deficit, but private sector doesn’t have that option. So under austerity we create a zero sum game.

Am I even making sense anymore ?

https://www.nytimes.com/2019/02/25/opinion/running-on-mmt-wonkish.html

103/ seems to me from reading this and some of the references that the disagreement seems to be “technical”. Krugman seems to agree that the fear of deficits is overblown, but seems to argue that interest rates are another tool to manage possible inflation. Tbh I haven’t gotten the opposite impression yet from the book, but maybe I missed it.

One thing I do wonder about is that if the deficit is in the form of bonds, won’t higher interest rates affect the cost of the accumulated deficit? Wouldn’t the public side now also have to pay more for the accumulated deficit? How does that work?

Maybe I don’t know how any of this works

105/ she is describing a model for interest rate that I think she is going to argue against. In it there seems to be a mechanism where one imagines that the private sector and public sector compete for loans in the same fixed sized market. And so the public sector deficits are in this model financed by loans in this market. And therefore the increased deficit would then be a significant increase in demand on a finite supply of money. And therefore drive the interest rate up.

But… that’s not how it works? In the real world? The banks increased their interest rates when the central bank did. So this model doesn’t make sense at all to me.

https://youtu.be/ZuXzvjBYW8A?si=g_1Z9XfgsTpioq2G

(h/t @Di4na)

Have the Boomers Pinched Their Children’s Futures? - with Lord David Willetts

https://social.vivaldi.net/@Patricia/112704863073553929

Patricia Aas (@[email protected])

4/ “Capital in the Twenty-First Century” by Thomas Piketty https://social.vivaldi.net/@Patricia/112681938811222913

https://www.ecb.europa.eu/press/key/date/2024/html/ecb.sp240626~0cdeaedbb1.en.html

114/ And here from the Congressional Research Service

Deficit Financing, the Debt,

and “Modern Monetary Theory”

https://sgp.fas.org/crs/misc/R45976.pdf

116/ But one thing I haven’t read much about is this inflation they’re currently fighting with interest rates globally. What do they think caused that? The EU guy didn’t seem to think it had anything to do with the financial measures during the pandemic, but rather fallout from the supply chain breakdown? I really need to read that speech more closely.

For Norway imo imported inflation of 2-3 percent doesn’t really matter when exchange rates mean that imports are 25(?) % higher than a couple of years ago. And I’ve realized that people aren’t distinguishing the two much in the media. But the interest rate hike that they are apparently doing to fight the insignificant inflation is killing households who are struggling with food prices due to the weak NOK.

For real. I don’t get the interest rate hike at all, it seems purely destructive for no reason. It clearly has zero effect on the value of the NOK.

117/ For real, how does this make any sense? Companies costs are increasing because the NOK is historically weak and interest rates shot up, so costs are way up and demand is way down. So their answer is to continue to beat Norwegian households into “submission” because they are already lying on the ground?

“There is uncertainty about the further development of the Norwegian economy. If companies' costs continue to rise rapidly or the krone becomes weaker than forecast, price inflation may remain high for longer than we currently envision. Then the committee is prepared to raise the interest rate again.” (Google translation)

https://www.norges-bank.no/kort-forklart/inflasjon/

https://youtu.be/fjoDjv1R3to?si=0jJNF-sEFAdFC8rR

Sellers Inflation [Isabella Weber]

https://youtu.be/RyIeC21XeLs?si=O7YOGfZd_ETpc8vR

Jon Stewart Forces Economist To Admit Capitalism Screws Us All

121/ Finished chapter 7 and 8 and it is pretty clear to me that this is mainly aimed at the US, and seems to be intended as an economic lever to shift the US in a more social democratic direction.

This is her summary of MMT

123/ I have been trying to find someone saying what is causing this inflation. And it's weird how little there is to find on this. But I found a page on the national statistical institute of Norway (SSB) talking about inflation in 2023. And it is really funny how they even point out the same feedback loops I've talked about in this thread (plus some more):

- rents are up (increased interest rates are probably a factor)

- imported goods are up (weak NOK is probably a factor)

Other things they brought up was that energy prices had been very high and that those losses were probably also being priced in.

The thing is... That means that we are turning up interest rates partially because we turned up interest rates and partially because our currency is weak and that energy prices were high a year ago. And turning up interest rates is not made to fix any of that.

It is made to cool down an overheated (too much money, too much spending) economy.

But that isn't what the economy looks like. But since they have reduced the entire state of the economy into one number (plus some including this, excluding that numbers), all context is gone and they pull out the same hammer that is part of the reason we got in this mess.

https://www.ssb.no/priser-og-prisindekser/konsumpriser/statistikk/konsumprisindeksen/artikler/kraftig-prisvekst-i-2023

Kraftig prisvekst i 2023

Året vi har lagt bak oss var nok et spesielt år når det gjelder prisvekst. I et historisk perspektiv steg prisene uvanlig mye. I motsetning til året før, da prisveksten økte kraftig for de fleste varer og tjenester som husholdningene kjøper, var bildet litt mer sammensatt i 2023.

124/ Their whole model is based on the assumption that when prices go up it is because demand is up. But sometimes prices go up because costs are up. And... that is not fucking supported.

I don't know what to say.

@Patricia Maybe it's what you're alluding to, but the big case of inflation without demand increase was '70s stagflation from the oil shock.

Conventional wisdom is that this was brought under control by high interest rates, despite the economy being weak (very painful). I'm sure you can find more subtle takes.

The lesson about avoiding stagflation is to maintain military supremacy over oil producers. ;)