47/ I don’t know what the answer is, my earlier idea of constraining the supply of NOK… it looks like they did that, and it had apparently about as much effect as the interest rate (not much if any).

Maybe without these two things it would’ve spiraled out of control… but I don’t think so, because this wasn’t caused by our economy.

So maybe the best thing would’ve been to just accept it? Yeah, the NOK is weak, because the world is rough, increase salaries some and just sit tight? Maybe even stimulate internal growth to compensate?

48/ And maybe the bottom dropped out from under the NOK, but the whole oil tax thing will keep it from dying. Because there will always be buyers, because they have no other choice.

49/ is it possible that they are so afraid of “inflation” they are actually creating “inflation”? (Where each “inflation” is a different flavor of inflation)

50/ I told you, inflation is much harder to grok than I thought, because it’s much less well-defined than they say it is. It seems economists don’t actually know what it is, they just know some of its shapes. Unfortunately, the current Norwegian shape is not the stereotypical one. And the Norwegian central bank only has one hammer and it was made for the stereotypical case.

51/ Ok, I’m still on the inflation chapter (but getting towards the end, I promise), and I think I get at least one of the major changes MMT wants to do: To manage the economy through fiscal policy: spending more/less and increasing/lowering taxes, instead of through monetary policy: raising/lowering interest rates.

52/ Ok, I think I get it. MMT says that a deficit isn’t a sign of government overspending, inflation is. (And here they are clearly talking about the overheated economy inflation) So as long as the spending doesn’t cause inflation, it doesn’t matter if you run with a deficit even over a longer period (she mentioned decades).

So basically she is sort of saying that deficits aren’t real because taxes aren’t real.

This is more like the water in a radiator system (my analogy). You can add in water or remove water, but the system isn’t the water. And adding water (money) only becomes a problem when the pressure in the system gets too high and water starts spilling out somewhere.

Basically, money isn’t “real”. It’s… just water in a radiator system in a building. The building and the radiators and the people living there are the real things.

53/ Ok, fine. Y’all have told me over and over to read Steve Keen, and I would’ve if he had a freaking audiobook, but he does have a podcast, so let’s do a crossover, because he has an episode on MMT.

(h/t

@joelving and the 5 other people who have brought it up)

https://mastodon.joelving.dk/@joelving/112720891429481986@[email protected] @[email protected] Most economic forecasting models are relatively simple and don't require supercomputers (because the models are oversimplified).

Steve Keen takes a System Dynamics approach and has many more feedback loops in his models. He's also one of the fiercest critics of mainstream economics I know of, for many of the same reasons @[email protected] is. Worth looking up, if it interests you.

54/ Hopefully the link to the episode works, title is “Does Modern Monetary Theory make sense?”

https://debunkingeconomics.com/episode/does-modern-monetary-theory-make-sense

Does Modern Monetary Theory make sense? | Debunking Economics - the podcast

Modern Monetary Theory states that’s, because the government of a country is the monopoly supplier of money, it has an unlimited capacity to pay for things and...

55/ Short recap: he basically agrees with MMT on most things. One thing came up though which is relevant to my discussion here about Norway, and that is that the USD is not a normal currency, and it can get away with a lot the rest of us can’t. The term he used was “reserve currency”.

https://en.wikipedia.org/wiki/Reserve_currency

Reserve currency - Wikipedia

56/ Here is the clip, I have no idea if he’s right or not about this particular argument, but I do think that (as far as I’ve gotten in the book) MMT seems very US centric and I also wonder if this protection they get from being a “universal global currency” protects them in ways they might not be completely aware of.

57/ The parts of MMT that I like are the descriptive parts. Where they just talk about How Stuff Works In Practice. The problem I have (and tbh they are by far the worst here) is that when they slip over from descriptive to prescriptive it’s like they don’t even notice. They go straight from How Stuff Works to My Opinion without skipping a beat. And then I start to wonder if they can even tell the difference.

58/ Another interesting clip from Keen where they talk about how to “create money”:

1. Through exports

2. Printing money

3. Borrowing from banks

59/ Ah nice, finally we have some mention of a more “global” economy. And this is where I want to learn more “trade deficit” vs “trade surplus” and how it interacts with currencies.

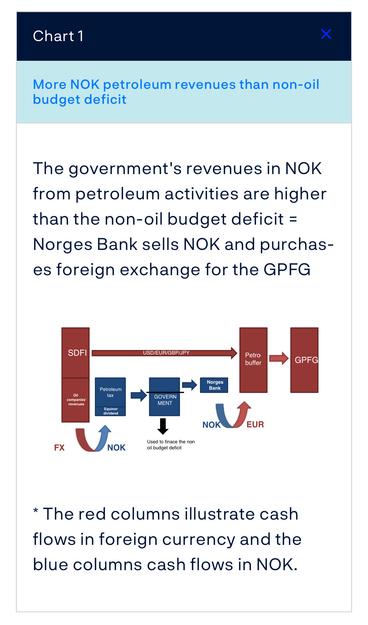

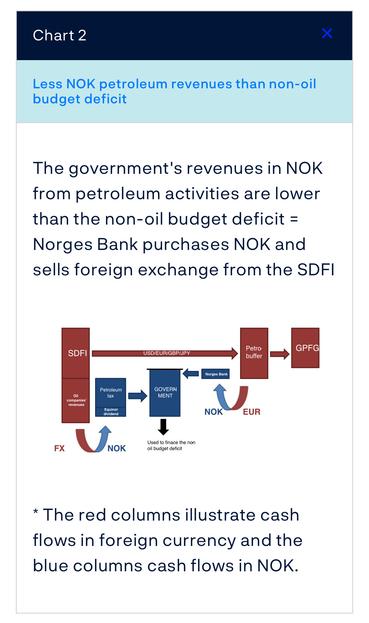

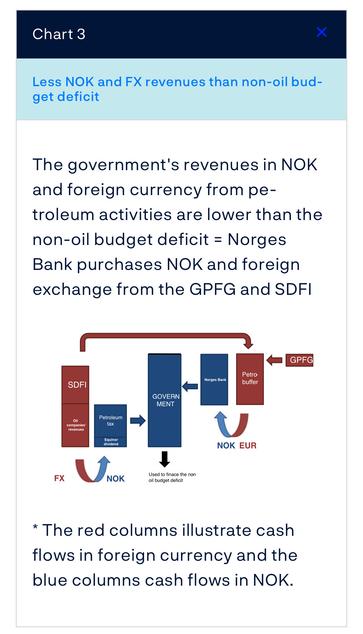

60/ someone asked about this buying and selling of NOK when it comes to the sovereign wealth fund. And the Norwegian central bank has a page on it in English! And it has pictures 😃

https://www.norges-bank.no/en/topics/liquidity-and-markets/Foreign-exchange-purchases-for-GPFG/Norges Bank’s foreign exchange transactions on behalf of the government

The Norwegian government receives revenues in both NOK and foreign currency from petroleum activities. Some of these revenues are used to finance a planned central government budget deficit. Norges Bank carries out the necessary foreign exchange transactions associated with petroleum revenue spending. These foreign exchange transactions are planned and smoothed over the year and are pre-announced each month.

61/ Based on this is it possible that Norway is actually doing MMT? Sort of? But instead of “printing money” they are covering a planned deficit with the earnings from its petroleum export?

62/ I feel so smart when I read news articles that agree with me 🤓 🤣

“And an interest rate increase will not help, he believes. - The higher the interest rate goes, the more landlords have to raise the rent, and then the interest rate increase is inflationary. It does not have the same effect as in the housing market, where prices fall if interest rates rise. The interest rate is not a good weapon to deal with this kind of inflation. It makes matters worse, he says.”

https://e24.no/norsk-oekonomi/i/93zl4d/uenige-om-leieprisene-det-gjoer-vondt-verre

https://social.vivaldi.net/@Patricia/112720508129615142

Uenige om leieprisene: – Det gjør vondt verre

Vil leieprisene knuse drømmen om rentekutt, eller har det lite å si? To sjeføkonomer er uenige om effekten.

63/ What is absolutely hilarious is that the effect he describes on the housing market is actually not happening. But this is yet another time the terrain is wrong for not fitting their map.

64/ Real estate prices are up 8% this year, that’s bananas. But I guess it’s like the gold, people are investing in their homes, and maybe also the fact that it is a closed loop system. So until people start defaulting on their loans, the real estate market won’t feel it.

65/ After spending ages on inflation, I’m apparently breezing through chapter 3 “The National Debt (That Isn’t)”

Basically, in the same way tax isn’t real (in that it is just a mechanism to remove money from the economy and/or create demand for the currency. MMT says that the deficit isn’t real. Very clear that it is the US they are talking about. To generalize to more countries she picked the UK and I would’ve preferred another more “normal” country.

66/ Ok, done with chapter 3, the above sums it up, maybe with an addition that she is very pro-deficit, to the point that she’d like to give it another name. The whole thing is very idealistic, and that part should probably have been discussed beforehand. Because in effect the ideology and The Plan is mixed in with what is presented as descriptive. And maybe it’s just me, but I like it when the agenda is very clear and when the shifts between what is claimed to be descriptive and what is prescriptive is clear and emphasized.

67/ To be fair, I think that issue is pervasive in the whole field. They are not able to separate ideology from models of the economy. And then they infuse in morality and destiny and Right and Wrong in these models until it’s more mythology than science.

And I don’t mind ideology. I have a great helping myself. But when you’re already in a non rigorous field, mixing opinions into “models” makes the whole thing even less serious.

A complex system is what it is. You find out the shape of it empirically. You can form hypotheses, design experiments and test. You don’t sit in a corner and Devine It. You might have a famous “shower thought” but then you test.

And seriously, these people (economists) don’t test ANYTHING.

68/ I really thought I’d be more convinced by leftist economists. But they are methodically all very similar. And it is the methodology I have issue with in this whole… project(?).

This field has imo structural issues and they aren’t fixed by the practitioner being less of an ass.

The problem is they believe in these simplistic models and that is standing in the way of developing the kind of tooling, discipline and humility needed when working with complex systems imo.

69/ anyway, next chapter: 4. Their Red Ink Is Our Black Ink

70/ Related to this, if you had a billion dollars and you were convinced that we were facing a climate catastrophe which might even be an extinction level event. Where would you put your money to try to save it (don’t say you’d give it away, because you didn’t become a billionaire by giving stuff away)?

https://social.vivaldi.net/@Patricia/112719504676456386When you quote me I hope you pick the best quotes: “And I posit that the NOK is weak because the planet is fucked and everybody knows it.”

https://social.vivaldi.net/@Patricia/112719497998588756

71/ Couldn’t get excited about chapter 4 and 5 seems so much more interesting because it is about trade.

72/ Finally had some time to continue and this chapter might take a while, and I might need to read it several times. Funnily it seems that she agrees that the dollar is special. I learned a thing, though, after the world abandoned the gold standard we kind of didn’t, we pegged the dollar to gold and a lot of the other currencies to the dollar. This was called the “Bretton Woods system”.

https://en.wikipedia.org/wiki/Bretton_Woods_system

Bretton Woods system - Wikipedia

73/ Well there it is, I wasn’t off base after all. Because of the position of the dollar the Feds actions, aimed at the domestic economy, has a much larger international blast radius.

74/ Some Norwegians have recommended that we peg the NOK to the Euro, and I think that our feeling that Denmark is similar to us culturally distracts us from recognizing how fundamentally different our economies are. Most importantly the petroleum “enhanced” economy of Norway and the fact that Denmark is a member of the EU and we are not, even with our extensive trade agreement.

75/ Chapter 5: “‘Winning’ at trade” is interesting, but doesn’t really go into the depth I’d like (but I guess after reading 4 Econ books in a row I’m not the target readership). The chapter is very “political” and idealistic rather than descriptive, but that was a tendency we saw earlier too. The basic idea is that a trade deficit isn’t a bad thing. She goes on to envisage a world economy that is more… equitable? It argues for developing countries to focus more inward, and diversifying their economies, perhaps making them less vulnerable to the global markets. It argues against losing control over one’s own currency (its MMT, so obviously). It makes clear that the dollar gives the US an outsized influence and leverage over the rest of the world.

She criticizes both democrats and republicans, but seems to have a soft spot for Bernie Sanders. He hired her to work at the Capitol, so I guess that makes sense.

The MMT premise seems to be that you don’t have to “have the money” to fund guaranteed full employment or “entitlement programs”, because the control over the currency means that the government always “has the money” to pay.

76/ The “winning vs losing” at trade is explicitly directed at Donald Trump. But she spends a lot of time emphasizing that American workers have lost jobs (“well paid union jobs” comes up several times) when production moved offshore.

It feels to me like she is arguing for a midpoint, a more protectionist approach, but not measuring in trade deficit/surplus, but instead in… standard of living?

She gets slightly into the topics of “The Shock Doctrine” in that the international trade organizations and the world bank became dominated by extremist (my word) capitalist forces.

77/ What I appreciate:

1. She is clear that the challenges that face us in the years to come are global, and that we have to work together to solve them, as partners instead of competitors.

2. She is not proposing some sort of bloody global revolution.

3. She is slowly selling me on the idea that guaranteed employment, benefits and entitlement programs are a safeguard against radicalization. I have mostly thought of these things as the “right thing to do” rather than a way to maintain peace.

4. The ideology is inclusive instead of divisive, and therefore doesn’t rest on the boogeyman approach of both the fundamentalist left and right. She doesn’t use immigrants or poorly veiled antisemitic tropes (the evil rich man of various formats) to paint some other group as the enemy.

78/ I think 4 is essential for progress to be made, because the current right and left political movements are focusing on targeting hate and animosity towards another group of humans, rather than at an inequitable system. And that only perpetuates that system because that energy is wasted on being unproductive (and hateful, which sucks the soul out of everyone at a time when we need a surplus of generosity, in my view)

79/ But the book is supposed to not just be a work of ideology, but provide a way through this mess we’re in, in the aftermath 🤞of a global economy dominated by extremist capitalism.

And that premise is based on this currency “trick”, and there I am not yet convinced tbh.

80/ Chapter 6 is on entitlement programs, but I think I’m going to go back to chapter 4, which I skipped, hoping that might be a bit more illuminating on the MMT side.

81/ why are we humans so ready to blame all of our problems on “the other”. With all that we know about the consequences of this, we seem to fall for it every time. Why do we let them make us fight each other in some grotesque gladiator game? Is it our need for simple solutions? Do we need someone to hate?

That train of thought reminded me of this Norwegian song

https://youtu.be/9QxGKTTtYgM?si=G9in1FTPPu2q49_a YouTube

YouTube82/ Norwegian lyrics:

“Han der er ikke sånn som deg

Fort deg bort og ta han

Det er like godt som sex

Å banke en stakkars faen

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Hør lyden av nakker som knekker

Hør lyden av kjøtt som sprekker

Det er bare å følge fingeren som peker

Dit hvor de voksne leker

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Han der er ikke sånn som deg

Fort deg bort og ta han

Det er like godt som sex

Å banke gørra ut av en stakkars faen

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?”

83/ Rudimentary English translation:

“He's not like you

Hurry over and get him

It's as good as sex

To beat a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Hear the sound of necks snapping

Hear the sound of meat cracking

You just have to follow the pointing finger

Where the adults play

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

He's not like you

Hurry over and take him

It's as good as sex

Beating the crap out of a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?”

84/ Ok, chapter 4 “Their red ink, is our black ink”. I think it was Keen in one of his podcast episodes who said something that I hadn’t considered. From memory: as a country’s economy grows, whatever that means, the money supply would need to grow too.

Looking at population growth alone that makes sense to me. And that means that my mental model of a fixed “amount of money we have” isn’t correct. It would, at least over longer periods of time, need to be elastic in some way. And I can’t see how that could be a global zero sum game either, since many countries that were poor a century ago, and are still poor today, often still have a “bigger” economy than they did a century earlier.

85/ So if “the amount of money” we have is flexible, and that the value of a currency is affected by similar forces as stocks and gold and whatever… that seems to support that money is “artificial”. And of course, economists would say “of course it is, we abandoned the gold standard ages ago”, but to me that hasn’t been obvious, because even if we don’t peg our currency to something tangible (directly or indirectly) that doesn’t mean that we can consciously “grow money” on a money tree.

86/ I can accept that the relationship with a currency is different when one has control of it, rather than being just a user of it. But it is nonobvious to me (still) that manipulating the money supply can be done largely with impunity. My brain (perhaps polluted by economics) feels that having more of something would make it less valuable. But maybe that’s not a universal law… maybe Maslow should have a say. If we take a consumable, perishable product that is a necessity through being food. Would having a lot of bread make it worthless? We still pay for bread, even when stores and bakeries throw away bread every day. So… maybe (bombshell 😂) the economic theory here is too simplistic? Maybe money doesn’t work the way we have been taught that it does?

87/ It’s funny because in my paper on Costa Rica (which I mentioned in another thread) one of the things that I argued was that what people believe (even if it is not currently true) is a driver for it to become true. So if a country started to print money at will, even if it might not matter (possibly 🤷🏻♀️) currency traders might believe that it does, and by the nature of their role, they might make it so it does matter, by weakening the currency through exchange rates.