82/ Norwegian lyrics:

“Han der er ikke sånn som deg

Fort deg bort og ta han

Det er like godt som sex

Å banke en stakkars faen

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Hør lyden av nakker som knekker

Hør lyden av kjøtt som sprekker

Det er bare å følge fingeren som peker

Dit hvor de voksne leker

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Han der er ikke sånn som deg

Fort deg bort og ta han

Det er like godt som sex

Å banke gørra ut av en stakkars faen

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?

Er det ikke deilig å ha noen å hate?

Føles det ikke godt å ha noen å hate?

Er det ikke herlig å slå dem flate?

Er det ikke deilig å ha noen å hate?”

83/ Rudimentary English translation:

“He's not like you

Hurry over and get him

It's as good as sex

To beat a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Hear the sound of necks snapping

Hear the sound of meat cracking

You just have to follow the pointing finger

Where the adults play

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

He's not like you

Hurry over and take him

It's as good as sex

Beating the crap out of a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?”

“He's not like you

Hurry over and get him

It's as good as sex

To beat a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Hear the sound of necks snapping

Hear the sound of meat cracking

You just have to follow the pointing finger

Where the adults play

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

He's not like you

Hurry over and take him

It's as good as sex

Beating the crap out of a poor bastard

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?

Isn't it nice to have someone to hate?

Doesn't it feel good to have someone to hate?

Isn't it great to knock them flat?

Isn't it nice to have someone to hate?”

84/ Ok, chapter 4 “Their red ink, is our black ink”. I think it was Keen in one of his podcast episodes who said something that I hadn’t considered. From memory: as a country’s economy grows, whatever that means, the money supply would need to grow too.

Looking at population growth alone that makes sense to me. And that means that my mental model of a fixed “amount of money we have” isn’t correct. It would, at least over longer periods of time, need to be elastic in some way. And I can’t see how that could be a global zero sum game either, since many countries that were poor a century ago, and are still poor today, often still have a “bigger” economy than they did a century earlier.

85/ So if “the amount of money” we have is flexible, and that the value of a currency is affected by similar forces as stocks and gold and whatever… that seems to support that money is “artificial”. And of course, economists would say “of course it is, we abandoned the gold standard ages ago”, but to me that hasn’t been obvious, because even if we don’t peg our currency to something tangible (directly or indirectly) that doesn’t mean that we can consciously “grow money” on a money tree.

86/ I can accept that the relationship with a currency is different when one has control of it, rather than being just a user of it. But it is nonobvious to me (still) that manipulating the money supply can be done largely with impunity. My brain (perhaps polluted by economics) feels that having more of something would make it less valuable. But maybe that’s not a universal law… maybe Maslow should have a say. If we take a consumable, perishable product that is a necessity through being food. Would having a lot of bread make it worthless? We still pay for bread, even when stores and bakeries throw away bread every day. So… maybe (bombshell 😂) the economic theory here is too simplistic? Maybe money doesn’t work the way we have been taught that it does?

87/ It’s funny because in my paper on Costa Rica (which I mentioned in another thread) one of the things that I argued was that what people believe (even if it is not currently true) is a driver for it to become true. So if a country started to print money at will, even if it might not matter (possibly 🤷🏻♀️) currency traders might believe that it does, and by the nature of their role, they might make it so it does matter, by weakening the currency through exchange rates.

88/ And as I mentioned earlier, maybe the dollar has some protection here. That through being a global “gold equivalent” everyone has a stake in it not tanking, even, I would guess, individual currency traders.

89/ Well, shit this is damning 😂

“Cases 5 and 6 underscore the lack of a causal relationship between rapid M2 growth [growth in money supply] and high inflation, because when we increase the threshold of nominal M2 growth to from 60 percent in five years to 200 percent in five years, it is followed by high inflation even less frequently than in Cases 3 and 4. This is, of course, the opposite of what one would expect if high M2 growth causes high inflation.”

(h/t @igimenezblb) https://www.ineteconomics.org/perspectives/blog/rapid-money-supply-growth-does-not-cause-inflation

“Cases 5 and 6 underscore the lack of a causal relationship between rapid M2 growth [growth in money supply] and high inflation, because when we increase the threshold of nominal M2 growth to from 60 percent in five years to 200 percent in five years, it is followed by high inflation even less frequently than in Cases 3 and 4. This is, of course, the opposite of what one would expect if high M2 growth causes high inflation.”

(h/t @igimenezblb) https://www.ineteconomics.org/perspectives/blog/rapid-money-supply-growth-does-not-cause-inflation

90/ I know after the rant I’ve been on the last few weeks that I shouldn’t be surprised that they just inferred from their damn models, with zero data to back it up… but shit I still am. Need to figure out if there has been discussions around this result.

91/ Oh here he goes into another side of this (very US centric): that the increase in household wealth as a result of deficits tends to be tied to real estate and stock values, and that results in wealth distribution inequality, because most poor people don’t own homes nor stocks.

https://youtu.be/wuonrlKefRM?si=7TUvGs-JeUI2AWW5

https://youtu.be/wuonrlKefRM?si=7TUvGs-JeUI2AWW5

The Paradox of Debt | Richard Vague | TEDxCapeMay

92/ As some folks have alluded at (where does the new money actually go) and based on something she says earlier in the book (that deficits have actually been too low) I started wondering. Imagine I have a truck full of dirt and I tell you I’m going to pour it out, you’d think it would create a pile of dirt, right? But what if I pour it into a hole. We don’t get a pile, we lose a hole…

The thing that I think MMT are arguing is that “debt” isn’t “debt” if it’s monopoly money you made up. To you as the money machine it behaves differently. And debt isn’t debt. It’s potentially pothole filling. But that means something is absorbing money, and don’t just say “rich people” because that is lazy. Are there holes? Where are they? What would be the effect of filling them? I’m assuming that filling different holes would have different effects. And maybe that’s MMTs thing: to fill the unemployment/underemployment hole? And from there achieve an effect?

93/ Even if we accept that money doesn’t work the way it works for us “money users”, for the “money creators”… and tbh that study was pretty darn convincing, I thought (I’d love to see an opposing view). Then… that doesn’t actually prove (in my mind) that all kinds of “holes” in the economy would behave the same when “filled”. Just because there isn’t a causal relationship between printing money and inflation, do we know what printing money actually does? And does it matter who gets it?

94/ Still in chapter 4. She was discussing another economist, Wynne Godley, and so I had to look him up and that opened another line on economic models: equilibrium models (the “mainstream economics” models) and a set of models referred to as “accounting models”.

Steve Keen, who a lot of folks have brought up (the guy with the podcast “Debunking Economics”) seems to be one of the people who are proponents of “accounting models”.

And it seems to me that MMT draws from the work of economists in this area.

Wynne Godley was credited for predicting the financial crisis based on his model.

This paper looks very interesting because it seems to contrast the two approaches. Which tends to be illuminating in my experience.

“No one saw this coming. Understanding financial crisis through accounting models”.

https://pure.rug.nl/ws/portalfiles/portal/2646456/09002_Bezemer.pdf

95/ so far my (quite shallow) understanding is that these “accounting models” model flows of money. With the basic premise that money has to come from somewhere and go somewhere. Or more accounting-wise that a subtraction one place has to lead to an addition of equal size (possibly the sum of multiple additions) somewhere else.

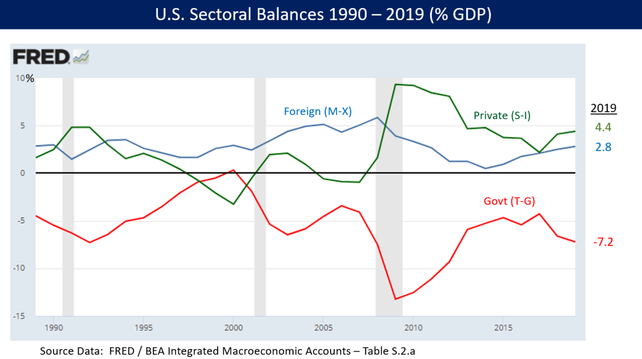

This relates to the idea that MMT presents, which Wynne Godley also seems to have supported and Richard Vague (above article and TED talk), that a deficit for the state necessitates a surplus somewhere else. Found this graph from Godley using his “sectoral financial balances” framework, depicting the US economy. This graph is very similar (perhaps identical?) to what Vague shows in his TED talk. They both show what seems to be an inverse relationship between a public deficit and a private surplus.

96/ I am worried that I’m finding this theory appealing just because the others are so terrible and so I’ve been primed to be positive to this one.

Which funnily enough is called “Anchoring effect” and features prominently in “behavioral economics”

https://en.wikipedia.org/wiki/Anchoring_effect

Which funnily enough is called “Anchoring effect” and features prominently in “behavioral economics”

https://en.wikipedia.org/wiki/Anchoring_effect

97/ Brains suck

98/ Ok, but if this is true, this seems to imply to me that austerity is counterproductive? That it would push an economy further into recession? Am I reading this wrong?

99/ my logic being that austerity means in effect a savings on the public side which would (in an accounting model) require “sucking” that money from other places in the economy, and that seems to mean mainly private sector. So to achieve plus on the public side using this mechanism would require minus on the private side.

100/ but hold up… I just argued that the size of the money supply was not fixed… but I guess that fits… because the public side can create money to cover it’s deficit, but private sector doesn’t have that option. So under austerity we create a zero sum game.

Am I even making sense anymore ?

101/ I’m sorry, but I have a lifetime of indoctrination to overcome here, and magic no consequences money tree seems a bit far fetched tbqh

102/ Ooh a rant against MMT by a Keynesian economist 🤓

https://www.nytimes.com/2019/02/25/opinion/running-on-mmt-wonkish.html

https://www.nytimes.com/2019/02/25/opinion/running-on-mmt-wonkish.html

103/ seems to me from reading this and some of the references that the disagreement seems to be “technical”. Krugman seems to agree that the fear of deficits is overblown, but seems to argue that interest rates are another tool to manage possible inflation. Tbh I haven’t gotten the opposite impression yet from the book, but maybe I missed it.

One thing I do wonder about is that if the deficit is in the form of bonds, won’t higher interest rates affect the cost of the accumulated deficit? Wouldn’t the public side now also have to pay more for the accumulated deficit? How does that work?

Maybe I don’t know how any of this works

104/ Also why reach immediately for interest rates? Is it because tax hikes are politically harder to pass? Interest rates seem to bring with them unintended consequences like increased profits for private sector banks and things like rent increases. In an inflationary economy I would think that the poor aren’t those “heating” things up.

105/ she is describing a model for interest rate that I think she is going to argue against. In it there seems to be a mechanism where one imagines that the private sector and public sector compete for loans in the same fixed sized market. And so the public sector deficits are in this model financed by loans in this market. And therefore the increased deficit would then be a significant increase in demand on a finite supply of money. And therefore drive the interest rate up.

But… that’s not how it works? In the real world? The banks increased their interest rates when the central bank did. So this model doesn’t make sense at all to me.

106/ Halfway through this but tbh this is a much more convincing argument for this phenomena than the pretentious colonial-envy drivel by Piketty. Young people are struggling because they are poorer than previous generations.

https://youtu.be/ZuXzvjBYW8A?si=g_1Z9XfgsTpioq2G

(h/t @Di4na)

https://youtu.be/ZuXzvjBYW8A?si=g_1Z9XfgsTpioq2G

(h/t @Di4na)

Have the Boomers Pinched Their Children’s Futures? - with Lord David Willetts

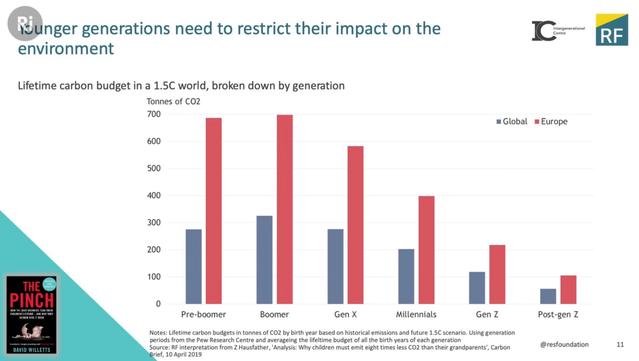

107/ I wonder if the distribution he is presenting is the same in other countries. Because according to him, boomers are consuming more than young people right now. And they are doing that from inside of their unmortgaged homes. Meanwhile young people get berated for being poor and are required to reduce their carbon footprint to a fraction (1/7?) of the boomers. Jeez.

108/ omg these numbers are mind blowing. Boomers are absolutely killing it. And young people are so screwed.

109/ Related/unrelated : Piketty pisses me off even more now. Because instead of just presenting the facts, I had to accompany him on his colonialist reminiscence tour. For data that is absolutely meaningless. Interspersed with the only woman he knows the name of, Jane Austen.

110/ if y’all are new here, you can experience my spiraling rage at Piketty’s Capital in that books thread (also linked to in my pinned thread of book threads)

https://social.vivaldi.net/@Patricia/112704863073553929

https://social.vivaldi.net/@Patricia/112704863073553929

Patricia Aas (@[email protected])

4/ “Capital in the Twenty-First Century” by Thomas Piketty https://social.vivaldi.net/@Patricia/112681938811222913

111/ oh my, I had forgotten how complete the Piketty-roasting Past Patricia did was 🧨🔥 good for her.

112/ Getting towards the end of chapter 4 (which I skipped earlier) and she’s talking about the crisis with Greece. And I have a question for EU folks: From a lot of these books I have gotten the impression, though maybe they haven’t gone out and said it, that Germany and perhaps France has an outsized influence/control over the Euro monetary policy. Is that accurate?

113/ This speech is very interesting and recent. Only a couple of weeks old. And also here the speaker, Philip R. Lane, member of the Executive Board of the ECB, seems to say that the relationship between growth of the money supply and inflation is not as clear as one used to think. This is very interesting… I think I need to read it more carefully.

https://www.ecb.europa.eu/press/key/date/2024/html/ecb.sp240626~0cdeaedbb1.en.html

https://www.ecb.europa.eu/press/key/date/2024/html/ecb.sp240626~0cdeaedbb1.en.html

114/ And here from the Congressional Research Service

Deficit Financing, the Debt,

and “Modern Monetary Theory”

https://sgp.fas.org/crs/misc/R45976.pdf

115/ I have read a lot from the aftermath of the financial crisis. And a lot of mainstream economists are all “Listen, inflation is too low, interest rates are also low and employment is high… and according to our models that isn’t possible.” And then they stop there. Can you imagine an actual scientific field that again and again had actual proof their models are wrong yet absolutely zero impulse to go: “ok, looks like this is all bullshit, maybe we should try to figure out how the system/economy actually works”

@Patricia Reading much of this thread, I finally remembered that I read "History of Greed" (by David E. Y. Sarna) some years ago. It isn't as much about economy as such, but examples of how markets of various kinds have been exploited since the early tulip days of Holland until the Bernie Madoff scandal. (and looking it up, turns out my description above is pretty much the sub--title of the book ...)

@Patricia Also, on the topic the financial crisis (I guess you may very well know this), The Black Swan by Nassim Taleb is more or less considered to have predicted the financial crisis of 2008. (Anecdote: I remember being in Seattle the late summer of 2007, seeing some slight worry at those sub-prime loans on the front pages of the local newspapers).

@larsivi it’s funny because my family and I did a road trip the summer of 2007, we drove from New York to the Florida Keys, and all the way we would hear commercials on the radio saying: “No Credit? Bad Credit? No Problem! We can get you a loan today!”

For us as Norwegians it was mildly absurd, but I guess we just assumed it was “an American thing”.

For us as Norwegians it was mildly absurd, but I guess we just assumed it was “an American thing”.

@larsivi I never did read the Black Swan. I always thought it was a business book

@Patricia I had it recommended to me by someone, and I'm pretty sure that person wouldn't have recommended a business book :) The book is more mathematical, on probabilities and how (very) unlikely, but high impact, events are handled in risk evaluations.

@larsivi as far as I understand it isn’t very technical, it was a New York Times bestseller, as far as I have gathered a “pop” business book

@larsivi but I guess it’s one of those books I have to read because I’ll know what people are saying, but where I almost always conclude that it could’ve (and should’ve) been a blog post

@Patricia I don't entirely remember, but it could have been a book I listened to rather than read. In any case, I liked it a lot back then, and doubt that I would if it was too long (although the points of it could of course almost certainly be condensed).