Signal and Noise

In my previous post I touched on the matter of discrimination in UK jobs markets:

In this one I will put together some data with sun dry commentary in order to straighten out the prevalent economic and markets narratives that in the mainstream perfectly blend in with bull market themes.

The outline is simple: we will spring off a couple of bitcoin forecasts.

Without ado, ahead of this we will establish three key risk factors to growth that stand in their own right:

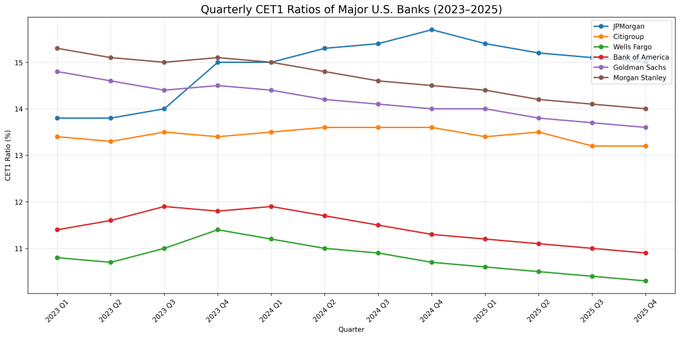

- The banks CET1 ratios dropping to limit credit growth

- Historically high corporate profits to GDP ratio to become inhibitive of growth: profits are taxes; albeit in part returned to equity holders just the same as a proportion of collected taxes is discharged toward welfare

- AI infrastructure buildout to hit a funding wall – potentially taking away the stimulus the economy relies on

In support of the first point, I asked ChatGPT to compile a chart!

Figure 1. Quarterly CET1 Ratios of Major U.S. Banks (2023-2025)

These seem approximately in line with my intuition from memory.

By the way, ChatGPT also takes credit for the feature image. I’d asked Claude too but it ran out of “messages” on both instances. I guess that due to effects of scale, in the first instance our original darling may have had the data ready in an API. Gemini fell behind, but owns the 200 character summary.

Now, don’t ask me where I heard the following (it was the financial media), but I am convinced the AI funding requirements of the US hyperscalers will in this year exceed their free cashflow. I placed a question mark on funding since private investment as a share of GDP is elevated.

With the risks in mind, shall we dive in?

Arthur Hays again shows just how much he doesn’t get it and goes on writing like a broken clock about “money printing,” this time as bond issuance explodes “to pay for wars” and provide UBI that will be required because “AI will replace 10-20% of w hite-collar knowledge workers.” He expects this will result in inflation and a break down of bond markets will cause central banks around the world to implement policies such as yield curve control. Amid this, his call is for bitcoin to hold 70k and then launch straight for the moon – fueled by the sheer increase in quality of “fiat” earning capped returns.

First, shall we take a moment to appreciate how it’s funny he’s certain a large deficit during what we can only assume would be a recession at least as severe as the GFC would cause inflation while the record wealth accumulation by capital markets participants and the associated surge in purchase power completely eludes him in this regard?

As we know, during the GFC unemployment peaked at ten percent like did the budget deficit. The problem the central banks consequently faced over the following decade was an absence of inflation. Post-Covid the story was complicated by supply chain disruption and the introduction of trade barriers, but the one defining characteristic of the recovery was “The Great Resignation” and the scarce availability of labour.

If the narrative could be reduced to the mechanics every bitcoin hothead recites – that of a huge amount of cash appearing, with relatively limited or no perceived reward to hold it – then indeed their expectations would make sense. This de-facto was so with the price of gold when “QE” was first introduced and later post Covid, with “QE-infinity.”

There obviously is the “nuclear” monetary policy response, but in order to trigger it we would have to actually enter into a major economic crisis. A significant loss of income occurring to those who are meant to “invest” in bitcoin as well as the possible decline of its real value in face of supply destruction would almost surely lead its price down at the first turn. Bitcoin is not detached from economic realities. I presented this argumentation consistently on this blog and Bluesky yet the crypto crowd chooses to cherry-pick which figments of reality to acknowledge.

While a “policy panic” of the kind outlined by Hayes is ultimately conceivable it’s certainly neither imminent nor immediately positive for the token.

Instead, we are almost certain to continue on the path of “gradual adjustment.” Here is a mention of Benjamin Cowen coining the term while recognising the full realities of bitcoin price formation. His call is for it to continue to depreciate toward 40k.

I note that on this path the risks outlined above may take us toward crisis sooner than the AI driven world grows recognisable.

In a previous post I gave a hot take on technology and AI from which we may extrapolate that the trend that will matter is one of consolidation. (Elevated M&A, anyone? GME/EBAY?) Critically, this isn’t a deflationary force.

Relatedly, as all currency is credit it’s the repayment of debt that creates a strong demand for it. Unless there is a wave of defaults – that aren’t offset by newly issued obligations by a third entity, such as a government – a currency should remain supported. On the other hand, defaults shed the cost of debt and after a one-time correction in the value of the currency occurs, cet. par. an economy carrying less debt will experience lower inflation.

Sufficient time has passed to assess the effects of the Fed rate cuts, tariffs alongside other MAGA policies, and AI. Since the funds rate was reduced from a range of 5.25% to 5.5% by a full percentage point between Aug 2024 and Jan 2025 – when Trump took office – until Aug 2025, unemployment edged up from an average of approximately 4.1% to 4.4% while core PCE averaged about 2.85% having pronouncedly dipped to a low of 2.615% in Apr 2025. Between Aug 2025 and Jan 2026 the Fed delivered an additional 75bps of easing taking the funds rate to the current range of 3.5% to 3.75%. After briefly surpassing the level, unemployment remains steady in the 4.3% to 4.4% range, while core PCE is in a clear up-trend (preceding the Iran conflict) and currently sits at 3.3%.

We see that inflation is much more accentuated than was anticipated by Wall St. back when strategists were evaluating the future effects of tariffs. E.g. Morgan Stanley’s expectations were core PCE would drop to 2.3% by now. In a post published at that time, having taken the fiscal austerity of the new administration into consideration, I argued that the immediate risks are deflationary but contrary to the MS analysis that significant inflation potential due to growth and tariffs remains “in the tail.” Both GDP and inflation developed much more in line with my own expectations. Of course, underestimating inflation played into their bullish equities estimates as well as aligned with administration rethoric. (Also, they’d said, there were going to be bunches of rate cuts.)

While the culprit for “transitory” inflation back then were tariffs, despite that I feel they haven’t yet fully factored in, now it’s energy.

The Powell Fed has consistently appeased Trump and added fuel to the fire of his tariffs. A central bank, I once thought, being the regulator of the currency must ensure there is sufficient liquidity in the system. Inflation can not occur without the monetary authority allowing the quantity of money to grow. In other words, I now recognise there always is enough liquidity in the system – the question just is at which level of prices, and employment.

The fact of the matter is that MAGA policies, along with to an as-of-now very minor extent AI, have pushed up the natural rate of unemployment. But, it’s chiefly the tariffs rather than AI that have put a cap on employment. Manufacturing in a country that places levies on input costs is less lucrative and this incentivises export-oriented jobs to move abroad.

As the science of economics knows well, any attempt to use monetary policy to guide unemployment below its natural level will result in inflation.

In all, the jobs market has not normalised, inflation has not cooled, neither productivity nor GDP have significantly grown (though GDP has more than Wall St. had projected), while corporate profits – well, are at risk.

Speaking of productivity growth, the metric declined through the second half of the Greenspan era and was slow to recover post the GFC. It seems to be somewhat positively correlated with interest rates. Corporate efficiencies, and profits, are found in employee’s markets, when employment grows most slowly and companies can’t simply throw in more employees to support their endeavours.

Which factors, then, will define our path of “gradual adjustment” and guide the markets?

Foremost it will be the development of productivity, employment and inflation in response to AI and the MAGA administration policies. As we have seen thus far, these have been quite ineffectual. The two key differences between the present circumstance and those following the GFC up to and including the period immediately before Covid, as well as the later half of the Greenspan era during the George W Bush presidency and the War on Terror are the inceptive level of unemployment and the embedded inflation expectations. I wrote previously that the simultaneous sustainment of both the equities and bonds bull markets depends on the prevalence of the impression of a tacit crisis. In such circumstances the expectation of (further) stimulus lifts both asset classes, while inequality grows, and the only obstacle can be if the condition were to somehow mistakenly appear fixed. It’s that the aggregate level of liquidity in the economy would be comprised more of, so to say, real liquidity rather than credit/stimulus which would bear consequence for the inflation outlook and then the prices of alternative numéraires. An economy accelerating due to real/secular drivers is fundamentally different than a stimulated one. Should the economy approach the condition of secular growth, I wrote, bonds will lose their appeal – on a prospective returns basis. Since private investment in AI infrastructure has become the main driver of growth, even if I am slow to pick up on the fact, we have entered precisely this pitfall. Due to the economy operating near full employment, as well as the inflationary backdrop the central bank finds its “headroom” diminished – which, in my opinion, will persist during the “gradual adjustment.” On the other hand, a disappointing outcome of AI trends could lead to a severe liquidity crunch.

I say this observing that a mini liquidity crunch has already, in a way, developed as the markets responded to the latest round of Fed easing with a drop in price of gold as well as a rise in yields. Money is in tight demand since highly profitable corporates have sucked it all in through earnings – only for others to want to circle back for more with upcoming AI IPO’s. What happens if we find out there isn’t enough to go around, at these prices?

Having discovered the drivers behind the macroeconomic trends, I guess what follows will, indeed, be late-cycle behaviour.

As previously discussed, we expect such slowing of the economy to coincide with the expansion of the liquid savings of the private sector relative to effective liquidity, indicating a rise in bearishness. The economy tweeds along looking for new ways to grow. A decline in (structural) inflation might enable a recalibration of rates and a positive adjustment of the investment schedule allowing the trend of (secular) bearishness to reverse.

Unless monetary policy stimulus comes with a further rise in bearish expectations raising the demand for money, the liquidity premia associated with alternative numéraires may rise above that of the currency, while should we find the stimulus to be substantial these premia may also elevate above those of bonds. A more hawkish Fed might first lead inflation lower and only subsequently provide more ample accomodation while a more doveish Fed might skip right ahead. This is the bet that highlights a scenario cet. par. bullish for bitcoin that need not necessarily be preceded by a major worsening of the economy – that of stimulus maintaining liquidity in an elevated band as immediately post the GFC or after the Fed ended its most recent tightening still allowing inflation to run hot.

I previously noted that in the scenario where monetary policy cannot possibly be effective the best possible course of action for the monetary authority – resulting in the optimal inflation and employment outcome – would be to attempt achieving what I dubbed “normalcy,” i.e. the relative stability of preference for the various nominal numéraires.

It would be supremely foolish for the Federal Reserve – as an institution that has accumulated over a century of policy making experience tasked with, as I currently see it, maintaining a minimum of social inclusion amid a sustained economic expansion – to allow itself to implode by relinquishing the one tool it has in its toolbox, i.e. the dollar, especially in face of catastrophic alternatives and (thus) clearly inferior policy frameworks.

Fortunately, expectation that the bonds and FX markets may aggressively contradict its tune might guide the Warsh Fed’s hand.

We take note of a word salad calling for the Fed to “maintain an open mind and lower rates” emulating Greenspan’s “resistance to premature rate hikes to foster non-inflationary growth.” (PCE is at 3.8% y/y.)

At present, the Fed is set to wait for inflation to ease before continuing to reduce rates. This would remove the possibility of overly excessive easing and go to maintain the present market regime. With a relatively stable monetary policy the prices of risk should in time revert to following the fundamentals. In my opinion, the “Golden Age” is long overdue – but this isn’t to say corporate earnings can’t stay at elevated levels relative to GDP, and hence grow in nominal terms. It’s plausible equities edge higher while bitcoin continues to stall.

Investment preferences can shift independently regardless of macro conditions.

But even with next to all positive catalysts exhausted, there is one factor that supports the bullish thesis and this is Trump’s “Crypto Reserve” to be funded with $20B annually (peanuts, I agree, compared to other outlays). This bailout fund, which by the way, of course, is pure socialism, viewed as a stock buyback is about one sixth the size of NVidia’s while the bitcoin market cap is about 29.5% of the world’s fifth most profitable and the most valuable company. This means that NVidia’s buyback is approximately 1.77 times larger when adjuated for scale. However, should sentiment continue to deteriorate this inflow might not be nearly enough to cover the outflows and a fresh hot potato might be left to a future Democratic Congress.

A regime that is delivering Balkans style corruption to the United States is increasingly unpopular so that after a long and a dark year and a half hope is in sight that America may break with populism and demagoguery inherent to the MAGA GOP.

To explore what happens beyond the immediate term and to conclude, we’ll visit Ben Cowen’s note.

But, before that, let’s have another look at the concept of liquidity-preference: the aggregate amount of currency the public would like to hold at any given moment. I noted previously it’s possible for it to decouple from the actual quantity of money in existence. This is our “demand for money” view. When liquidity-preference is below the quantity available we expect to encounter inflation and especially that of the price of gold or bitcoin and vice-versa. In terms of motives for holding the currency this is reflected in the size of the residual, which exactly is the difference between the quantity of money available and liquidity-preference. When it’s large we can say that demand for money is low and vice-versa. Under normal monetary conditions the residual should be close to zero.

As well, to set historical context, let’s note that bond and equity markets are in general positively correlated.

Further, we can take a view that has thus far eluded us on this blog – of bitcoin as a currency. Recall, these trade on expected bond yield differentials. Hence, rising yields are adverse for bitcoin just as they have historically been for equities and gold. However, in the converse, equity prices will rise as domestic bonds sell off and their yields rise only when the markets are expecting heightened inflation. On the other hand, declining yields go in hand with secular bull markets enabled by fiscal discipline and sound money (the supply of which can expand using the bonds themselves as collateral) reflected in stable, well-anchored inflation expectations. The most stark example of this kind of an environment was the Clinton economy under Fed Chair Greenspan’s middle terms. Again to the contrary, equity bear markets will span a rally in bonds only if inflation expectations are pronouncedly declining or a monetary stimulus is either expected or enacted.

The positive correlation between bonds and equities can break if the Fed is seen to be “behind the curve.”

The liquidity premia associated with each of the assets (or asset classes) certainly can evolve independently of each other.

As we noted, the critical factor is the unemployment rate since inflation most acutely develops when businesses must compete for workers by raising wages. Both the Clinton and Obama economies had ample unemployment “headroom” inherited from their GOP predecessors – which they were steeply reducing throughout, accompanied by a strong growth in private investment as well as the afore-mentioned fiscal discipline and firmly anchored inflation expectations. The trade-off was slightly lower corporate profitability. Admittedly, the economy may have suffered during the late years of the Clinton presidency as the burden of sustaining the budget surplus excessively dragged on corporates. Their GOP successors attempted to “fix” such economies (found near full employment) by stimulating them with reduced taxation to boost said corporate profits. (Again, I touched on the mechanics in an earlier post.) The Trump GOP layers trade protectionism on top to additionally support the pricing power of the domestic corporates by shielding them from foreign competition. Thus, in Democratic economies you can afford to buy things while in GOP economies you need to borrow to fund your spending. Presto! We get: inflation, rising corporate profitability and moderating employment. The Powell Fed through its new average inflation targeting framework opted to prioritise employment and hold interest rates low. (It was adopted in 2020 and superceded last year.) This was the outline of our state of permanent tacit crisis in which monetary policy supports both bond and equities bull markets, while inequality grows. The Biden economy suffered the unfortunate fate of owning the post-Covid inflation spike super-imposed with the consequences of Trump’s tariffs which had caused the “affordability crisis,” that now he’d come back to fix – with more tarrifs and shouts for rate cuts.

Now, in Cowen’s work Figures 4. – 8. show the US eqity market has decoupled from – drum-roll, please – employment. This is the “nothing matters” rally, that persists as our tacit crisis was undone yet policy still goes on trying to resolve it. The decoupling can be a clear sign of one thing no one likes to hear about: a bubble.

I myself grossly underestimated the capacity for corporate profits to rise, but this doesn’t mean these can rise without end (as percentage of GDP). Historic pattern shows when this indicator starts falling a recession soon follows, with both its severity and proximity proportional to the steepness of the fall. A “gradual adjustment” thus supposes an absence of shocks and cet. par. an as-share-of-GDP rise in either of the following: taxation, compensation, or realised corporate investment net of the other two categories that includes both deprecation costs to replace expended resources, e.g. equipment or unrenewable energy sources, and the cost of acquiring new ones. On this blog, referencing Keynes, I argued that an increase in taxation is possible without a fall in output if the public decides to reduce their savings rate, i.e. increase spending as a portion of their income. But, low consumer confidence and deteriorating employment make both this and a rise in wages less likely – though the circumstances could change under a new political doctrine. Hence, a continued rise in realised corporate investment is left as the driver of growth. The limits of credit growth notwithstanding, we see that it’s strange to expect both corporate profits and investment to expand on a share of GDP basis without this becoming entirely detrimental, on the same basis, to compensation or tax receipts. The growth of GDP to maintain solvency in these left-behind sectors would need to be much larger than is currently projected – which highlights the pending unsurprising collapse of Miran’s MAGA fantasy budget. Companies will not invest unless there are prospects of profits. When deprecation increases, profits decrease.

Recall Wall St. just recently claiming the “growth premium” embedded with tech stocks had fallen “below market average” and we had a laugh how technically clumsy that formulation is? These people will say anything!

Consider whether it’s possible the “gradual adjustment” comes with a stall in the rise of corporate profits and this translates into an unwind of market momentum and de-leveraging that in turn spills over into the real economy by erasing the wealth effect or possibly worse – causes a Black Swan event?

The clock for AI to come through is ticking. The markets turn, let’s remind both the crypto and stocks bulls, on shifts in expectation and these happen quickly.

I previously referred to the scenario of high growth and low inflation as “fantasy pulp.”

If we take the view that businesses will compete among eachother to deliver products and services of the highest quality – by providing additional and more refined features – while maintaining a price envelope, then AI fails to deliver an increase in nominal profits. The price of material inputs to physical products is unlikely to decrease. People are already saturated with digital products. If AI is to mean an increase in volume of digital activity, if it’s to mean added processes for the afore-mentioned sake of refinement, then it will merely add cost. Together with the cost of infrastructure someone will have to pay for it all. A further rise in profitability can occur if businesses are able to make the same offerings at a reduced cost. However, the producer prices tell a different story.

Your flight to Zimbabwe is fully on schedule.

Let’s conclude by wishing the new Fed Chair a patch of good visibility, and plenty of success!

You got this Kevin!

#AI #banks #Bitcoin #CET1 #crypto #Economics #Economy #Fed #finance #inflation #interestRates #Investing #MAGA #Markets #Miran

雑誌付録ダイアリー【発売予定・レビューブログ】

雑誌付録ダイアリー【発売予定・レビューブログ】