94/ Still in chapter 4. She was discussing another economist, Wynne Godley, and so I had to look him up and that opened another line on economic models: equilibrium models (the “mainstream economics” models) and a set of models referred to as “accounting models”.

Steve Keen, who a lot of folks have brought up (the guy with the podcast “Debunking Economics”) seems to be one of the people who are proponents of “accounting models”.

And it seems to me that MMT draws from the work of economists in this area.

Wynne Godley was credited for predicting the financial crisis based on his model.

This paper looks very interesting because it seems to contrast the two approaches. Which tends to be illuminating in my experience.

“No one saw this coming. Understanding financial crisis through accounting models”.

https://pure.rug.nl/ws/portalfiles/portal/2646456/09002_Bezemer.pdf

95/ so far my (quite shallow) understanding is that these “accounting models” model flows of money. With the basic premise that money has to come from somewhere and go somewhere. Or more accounting-wise that a subtraction one place has to lead to an addition of equal size (possibly the sum of multiple additions) somewhere else.

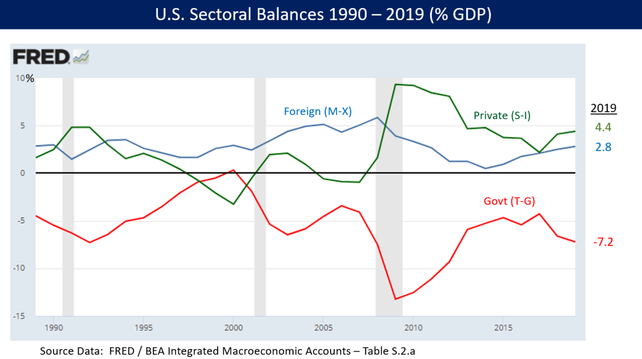

This relates to the idea that MMT presents, which Wynne Godley also seems to have supported and Richard Vague (above article and TED talk), that a deficit for the state necessitates a surplus somewhere else. Found this graph from Godley using his “sectoral financial balances” framework, depicting the US economy. This graph is very similar (perhaps identical?) to what Vague shows in his TED talk. They both show what seems to be an inverse relationship between a public deficit and a private surplus.

Which funnily enough is called “Anchoring effect” and features prominently in “behavioral economics”

https://en.wikipedia.org/wiki/Anchoring_effect

100/ but hold up… I just argued that the size of the money supply was not fixed… but I guess that fits… because the public side can create money to cover it’s deficit, but private sector doesn’t have that option. So under austerity we create a zero sum game.

Am I even making sense anymore ?

https://www.nytimes.com/2019/02/25/opinion/running-on-mmt-wonkish.html

103/ seems to me from reading this and some of the references that the disagreement seems to be “technical”. Krugman seems to agree that the fear of deficits is overblown, but seems to argue that interest rates are another tool to manage possible inflation. Tbh I haven’t gotten the opposite impression yet from the book, but maybe I missed it.

One thing I do wonder about is that if the deficit is in the form of bonds, won’t higher interest rates affect the cost of the accumulated deficit? Wouldn’t the public side now also have to pay more for the accumulated deficit? How does that work?

Maybe I don’t know how any of this works

105/ she is describing a model for interest rate that I think she is going to argue against. In it there seems to be a mechanism where one imagines that the private sector and public sector compete for loans in the same fixed sized market. And so the public sector deficits are in this model financed by loans in this market. And therefore the increased deficit would then be a significant increase in demand on a finite supply of money. And therefore drive the interest rate up.

But… that’s not how it works? In the real world? The banks increased their interest rates when the central bank did. So this model doesn’t make sense at all to me.

https://youtu.be/ZuXzvjBYW8A?si=g_1Z9XfgsTpioq2G

(h/t @Di4na)

Have the Boomers Pinched Their Children’s Futures? - with Lord David Willetts

https://social.vivaldi.net/@Patricia/112704863073553929

Patricia Aas (@[email protected])

4/ “Capital in the Twenty-First Century” by Thomas Piketty https://social.vivaldi.net/@Patricia/112681938811222913

https://www.ecb.europa.eu/press/key/date/2024/html/ecb.sp240626~0cdeaedbb1.en.html

114/ And here from the Congressional Research Service

Deficit Financing, the Debt,

and “Modern Monetary Theory”

https://sgp.fas.org/crs/misc/R45976.pdf

116/ But one thing I haven’t read much about is this inflation they’re currently fighting with interest rates globally. What do they think caused that? The EU guy didn’t seem to think it had anything to do with the financial measures during the pandemic, but rather fallout from the supply chain breakdown? I really need to read that speech more closely.

For Norway imo imported inflation of 2-3 percent doesn’t really matter when exchange rates mean that imports are 25(?) % higher than a couple of years ago. And I’ve realized that people aren’t distinguishing the two much in the media. But the interest rate hike that they are apparently doing to fight the insignificant inflation is killing households who are struggling with food prices due to the weak NOK.

For real. I don’t get the interest rate hike at all, it seems purely destructive for no reason. It clearly has zero effect on the value of the NOK.

117/ For real, how does this make any sense? Companies costs are increasing because the NOK is historically weak and interest rates shot up, so costs are way up and demand is way down. So their answer is to continue to beat Norwegian households into “submission” because they are already lying on the ground?

“There is uncertainty about the further development of the Norwegian economy. If companies' costs continue to rise rapidly or the krone becomes weaker than forecast, price inflation may remain high for longer than we currently envision. Then the committee is prepared to raise the interest rate again.” (Google translation)

https://www.norges-bank.no/kort-forklart/inflasjon/

https://youtu.be/fjoDjv1R3to?si=0jJNF-sEFAdFC8rR

Sellers Inflation [Isabella Weber]

https://youtu.be/RyIeC21XeLs?si=O7YOGfZd_ETpc8vR

Jon Stewart Forces Economist To Admit Capitalism Screws Us All

121/ Finished chapter 7 and 8 and it is pretty clear to me that this is mainly aimed at the US, and seems to be intended as an economic lever to shift the US in a more social democratic direction.

This is her summary of MMT

123/ I have been trying to find someone saying what is causing this inflation. And it's weird how little there is to find on this. But I found a page on the national statistical institute of Norway (SSB) talking about inflation in 2023. And it is really funny how they even point out the same feedback loops I've talked about in this thread (plus some more):

- rents are up (increased interest rates are probably a factor)

- imported goods are up (weak NOK is probably a factor)

Other things they brought up was that energy prices had been very high and that those losses were probably also being priced in.

The thing is... That means that we are turning up interest rates partially because we turned up interest rates and partially because our currency is weak and that energy prices were high a year ago. And turning up interest rates is not made to fix any of that.

It is made to cool down an overheated (too much money, too much spending) economy.

But that isn't what the economy looks like. But since they have reduced the entire state of the economy into one number (plus some including this, excluding that numbers), all context is gone and they pull out the same hammer that is part of the reason we got in this mess.

https://www.ssb.no/priser-og-prisindekser/konsumpriser/statistikk/konsumprisindeksen/artikler/kraftig-prisvekst-i-2023

Kraftig prisvekst i 2023

Året vi har lagt bak oss var nok et spesielt år når det gjelder prisvekst. I et historisk perspektiv steg prisene uvanlig mye. I motsetning til året før, da prisveksten økte kraftig for de fleste varer og tjenester som husholdningene kjøper, var bildet litt mer sammensatt i 2023.

124/ Their whole model is based on the assumption that when prices go up it is because demand is up. But sometimes prices go up because costs are up. And... that is not fucking supported.

I don't know what to say.

https://no.wikipedia.org/wiki/Norges_statsgjeld

https://youtu.be/0G6obeUKWmw?si=-rW1dPklrdytZCMz

How Do We Fix The Economy? Modern Monetary Theory, Explained | The Problem With Jon Stewart Podcast

129/ Ok, I had an epiphany.

And it’s about all the money that goes to the rich/banks. Where does it go? Because we don’t see it much in the real “normal” economy. (Or at least I thought so)

So what if, when we double or triple the money supply, but only/mostly give it to the rich/banks, we actually see inflation, but we didn’t recognize it as inflation?

What if the goods that got hit with inflation were “Capital” - that is real estate and stocks etc.

What if what we think of as capital gains is actually inflation on rich people stuff?

And maybe when rich people got a lot of money they spent it, but they spent it on rich people stuff?

Like apartment buildings.

And back to Harvey/Marx’ definition of “use value” vs “exchange value” - their money 💰 inflated the “exchange value” of real estate. Which is why nobody can afford a home anymore.

So basically the rich have their own economy, which shares its currency with us. But the stuff they can buy, at the scale they are at, are different things. We would perhaps get a nicer couch or more food if we got a lump sum in our scale (2000$ for example). They buy real estate and stocks at their scale (2.000.000$).

So you don’t see the inflation on groceries, but real estate values go up (or don’t go down).

130/ Which reminds me of a story a guy told me. So his building only had one electricity meter (I’m assuming it’s old), and so they had a practice of splitting the bill evenly between the units. But suddenly they had gotten a massive bill, 10-20x what they usually got. Turns out one of the units had started up a pot farm and apparently this was pulling a lot of energy for heating lamps or something (look I don’t know anything about growing pot). But since they only had one meter they had to split it anyway.

Or in my radiator system metaphor, what if one of the units had connected a pipe to the system and was siphoning off the water into the system next door? It’s a separate system. So our system would have this “weird quirk” where we filled and filled with water/money, but it never became over-pressurized. But if we filled a bit too much on a part of the system that bypassed this guys unit, then we actually saw over-pressurizing on occasion.

However, next door, they had to remove water regularly because it was constantly becoming over-pressurized from the continuous stream of water.

My brain is visual 🤷🏻♀️

https://youtu.be/m4MahOuEdVw?si=gisQblyM__PZGdTC

How Can We Fix Inflation? With Economist Steve Hanke | The Problem With Jon Stewart Podcast

133/ Lol, I’m still stuck on inflation. Remember way in the beginning of this thread when I said I’d be done with it soon? Well, here we are, way after the end of the book and I’m still stuck on inflation.

The problem is that inflation is like colic. If you ask people what colic is they’ll say something about stomach issues. But when you look up the actual diagnostic criteria it’s (for Norway): baby cries more than 3 hours a day, more than 3 days a week for more than 3 weeks.

So would it surprise you when I tell you about a study on kids that were diagnosed with migraines as children, one of the findings was that every single one had been diagnosed with colic as babies?

You have one single metric: baby cries.

IT COULD BE LITERALLY ANYTHING

(I’m clearly not annoyed by this)

So back to inflation. They have basically a shopping cart of stuff. And if it costs more then they say INFLATION. But why does it cost more?

Friedman (their hero) literally says that inflation happens (partially?) because people think it will happen.

I just can’t. This “field” is driving me nuts. It’s a wandering self fulfilling prophecy.

134/ Maybe some went up because their costs were up when rebooting their supply chains after the pandemic, maybe some went up because costs went up because of war (wheat in Ukraine), maybe some went up because of weaker currencies, maybe some went up because THEY RAISED THE INTEREST RATE, maybe some went up because… Everybody Else Did It And If We Do It Too Maybe We Can Make Some More Money???

But hey. We have one variable in our high school math equation. So fuck all of you.

😬🥳

135/ You know, one of the upsides of having more diversity in your field is new (and better 😇) metaphors, my gift to you:

Inflation is like colic

You don’t know why the baby/economy is crying

@Patricia and then you try to fix it with unproven home remedies. Sometimes it goes away by itself at the same time as you treat it so that must show that the remedies work....

My god, you're right!

136/ I give up. Norwegian inflation went down more than projected, so now Norwegian economists are predicting interest rate hikes 🤯Wait what? Reason: the NOK got even weaker. Wat? Well, you see, since the Norwegian economy looks like it’s going better than expected, people think we’ll lower the interest rate so then NOK isn’t that interesting anymore so… 🤪

This is such a bullshit field, no other field would get away with this crap. They just gaslight you constantly.

https://e24.no/norsk-oekonomi/i/MnnAxK/kronen-svekker-seg-videre-reell-fare-for-renteheving

137/ This is a joke. They’re just doing the economics equivalent of techno-babble. “Well, actually, the NOK is weak because inflation is low”

Fuck you, Mr Economist, y’all said the opposite a month ago.

Just say it like it is: WE DON’T KNOW, BECAUSE WE DON’T KNOW HOW THE ECONOMY WORKS, WE’RE JUST FAKING IT

Economics is not only a pseudoscience, economists are rude and condescending

https://borsen.dagbladet.no/nyheter/svakeste-pa-24-ar/81685750

138/ Why is it my problem that they created a completely unsuited academic discipline to deal with a complex adaptive system? Why is it my problem that they don’t even realize that they are dealing with a complex adaptive system? This is like the Middle Ages. It’s all weird superstition and using retrospective correlations to “show” they were right. Just say every single thing and then cherry pick your statements after the fact.

This is how con artists and carnival psychic’s work.

DO ACTUAL SCIENCE.

This is embarrassing for all of us.

@Patricia I mean they had entire wars about this. I guess the bad guy won.

139/ Ref post 129: I’m watching the documentary “97% owned” about the British monetary system and there they say this explicitly: increased money supply inflates housing prices.

But they also talk about why this is true (they are speaking about the British system, I don’t know if this is the case for other countries):

Most of the increase in the money supply is done by banks “printing money” where they lend out money they don’t actually have, even fractional backing for.

And since the only way they can “print money” is through new loans and since mortgages are much less risky in comparison to business loans, they “print money” by granting mortgages thereby causing inflation in a very limited part of the economy: the housing market

https://youtu.be/XcGh1Dex4Yo

140/ Something I didn’t know: the author of The Deficit Myth, Stephanie Kelton, was on an 8 person advisory economics working group for Biden and had a lot of influence on the economic policies to get the US out of the pandemic recession.

https://youtu.be/4BAsZIHp9HI

142/ So I’ve been thinking, if it is the case that increases in the money supply has led to inflation in housing prices (among other things). And if that increase in the money supply is driven through and/or created by private banks. What would be a solution for Norway? (Possibly other countries, but that’s harder for me to say)

The primary goal would have to be to remove real estate (mortgages) from the menu of financial instruments available for the banks.

Back to the use value vs exchange value: the use value of a house is its value as a home for people. The exchange value should not be available for speculation.

So how could this be done?

I don’t see another way than to take mortgages away from private banks.

In Norway student loans are public, run through an institution called “Lånekassen” (the loan box?), and we also have another “public bank” called “Husbanken” (literally The house bank). Today it handles a quite small part of the market, but imagine that it becomes dominant, offering the lowest rates, humane policies like loan freezes etc that the student loan bank offers today.

The state would in effect take over the mortgage market.

Private banks would have to lend out money to for example businesses. Which might perhaps make VCs less interesting.

@Patricia One solution is a land value tax:

* Most of the value of property is in land and it’s unearned

* Land can’t move or be removed as a reaction to the tax

* Do it the other way round: use LVT to take excess money out of the economy

* Disincentivizing speculation (you’re taxed for the full value of the land anyway) will cause more housing to be built

@Patricia I know there are a lot of things attached to it but I don't believe anybody should "own" land.

Given that nationalizing land leads to some really bad situations something like LVT or COST is a next best alternative (basic forms of these are used in cities around the world): https://www.flightfromperfection.com/the-common-ownership-self-assessed-tax.html

@Patricia Sure you can consider it unfair. People in Amsterdam also consider the leasehold system there to be "unfair".

But maybe allowing a single person and their lineage to monopolize a piece of land in perpetuity is unfair towards everybody else?

1) when you raise interest rates, you are increasing how much you are paying out in interest on your bonds. And if you have a lot of bonds this payout can itself cause inflation, but the payout is also unevenly distributed, it goes to the folks who own bonds.

2) raising interest rates will cause price increases in all products that are directly or downstream affected by inflation. (This has become clear to me ref the rent discussion up this thread)

3) when inflation goes up you have to increase the money supply by the same percentage or you are effectively shrinking the economy: if something cost x before and it’s now 2x that means you need twice the money for the same thing.

4) Tariffs are inflationary (which seems obvious but is not always discussed)

- not mentioned by him, but I’ve talked about: a weak currency is also inflationary

https://youtu.be/e-VC5Dfd4_A

I know something several people propose is having a large amount of public housing since the government isn't setup to do speculative investments. Vienna is the famous example of a city with a very large supply of public housing. The flip side is that you're kind of trusting that a right wing party doesn't come into power and sells off that housing because of x or y reason.

145/ Oh this is interesting:

“The European Central Bank (ECB) published a study showing that QE in the Eurozone primarily contributed to an increase in the wealth of the richest 20% of the population. Additionally, a report by the UK Parliament’s House of Lords Library stated that QE is likely to have exacerbated wealth inequalities in the UK. However, it noted Bank of England analysis concluding the effect was relatively small. Research published in the Oxford Bulletin of Economics and Statistics found that expansionary QE via asset prices led to net wealth inequality increases on some (but not all) metrics for most countries under review.”

(h/t @_dm) https://adepteconomics.com.au/does-quantitative-easing-primarily-benefit-the-wealthy/

Does Quantitative Easing primarily benefit the wealthy? - Adept Economics | Decision Defining Insights

With aggressive fiscal and monetary policy responses to the 2008 financial crisis and the COVID-19 pandemic, new evidence has emerged of the unintended consequences of activist macroeconomic policies. This article considers the impact of Quantitative Easing (QE) on wealth inequality. QE is an unconventional monetary policy used by central banks such as the US Federal … Continue reading Does Quantitative Easing primarily benefit the wealthy?

146/ It seems to me that things created for rich people to save are the root of most evil here. I don’t really care if rich people are rich, but if their piggy banks are killing the rest of us that’s a problem.

Scenario: you are loaded. Where to put all of this money?

1) bank account: low interest

2) government bonds: low interest

3) stocks, a synthetically created instrument: we have split up the ownership of companies into tiny NFTs that can be traded, used for control and might give some payouts

4) real estate, both homes and financial instruments: the use of it as a financial instrument inflates the price of them as homes

Number 3 is basically the center of the book The Unaccountability Machine: “optimizing for shareholder value” (Friedman, of course) causes companies to behave in ways that are contrary to long term sustainability, both for the company and the planet.

https://social.vivaldi.net/@Patricia/112837112508276909

Patricia Aas (@[email protected])

139/ Ref post 129: I’m watching the documentary “97% owned” about the British monetary system and there they say this explicitly: increased money supply inflates housing prices. But they also talk about why this is true (they are speaking about the British system, I don’t know if this is the case for other countries): Most of the increase in the money supply is done by banks “printing money” where they lend out money they don’t actually have, even fractional backing for. And since the only way they can “print money” is through new loans and since mortgages are much less risky in comparison to business loans, they “print money” by granting mortgages thereby causing inflation in a very limited part of the economy: the housing market https://youtu.be/XcGh1Dex4Yo

1. Cash is expensive to produce, the government wants to reduce that cost; therefore they encourage cashless

2. Cash is expensive to handle, banks don't like the hassle and pass cost on to retailers, who prioritise cashless to reduce costs

3. Governments like to be able to surveil what people do with money, electronic payments permit that, cash doesn't; therefore they encourage cashless more

@mrsbeanbag @Patricia @janl UK banks are subject to Capital Requirements these days rather than Reserve Requirements which achieves much the same objective but with measures and accounting that much more reflects the modern ways of controlling lending & risk

"Capital requirements govern the ratio of equity to debt, recorded on the liabilities and equity side of a firm's balance sheet. They should not be confused with reserve requirements, which govern the assets side of a bank's balance sheet"

@Patricia

The norges bank has an explainer on their website. Its much the same as elsewhere, with Norwegian details.

You can look at figure 2.4. The purple block is deposits in banks. Customers consider that as 'money'. The light grey on the asset side is claims on the CB. That's 'base' money 'printed' by the CB.

The rest of the purple is backed by assets that are valuable but not money. Thats the maturity transformation, where the banks 'turn' not-money into money

@mrsbeanbag @Zamfr @Patricia you don’t get repo’d for a single payment miss lol. I don’t know exactly what the line is, Google suggests 120 days.

Lenders don’t like foreclosing on stuff, it’s bad for business.

But obviously the bank will call you and probably look at refinancing if you suddenly stop paying your mortgage. When you look at the properties that are sold by the mortgage lenders it is obvious that there was other stuff going on with these owners.

@mrsbeanbag @Zamfr @Patricia So the banks just stopped repossessing homes and the we had zombie mortgages sometimes for years.

Some folks got back on their feet and were ok, I don't know what the numbers panned out like in the end though.

This is a pretty crazy story though: https://www.npr.org/2024/05/10/1197959049/zombie-second-mortgages-homeowners-foreclosure

https://youtu.be/MLKrBsTQntA

@Patricia so giving out a lot of mortgages is fine. As long as folks are actually credit worthy and your not allowing leverage.

This is why strong regulation is critical b/c of course banks will always take more risk if they can.

Mortgages given out w/ proper risk management should not led to undue inflation.