“ BY CHRISTOPHER RUGABER

Updated May 26, 2026 9:05 AM

WASHINGTON (AP) — U.S. consumer confidence declined slightly this month as gas prices stayed high and inflation remained elevated, a sharp contrast to soaring stock prices hover near record levels. The Conference Board’s consumer confidence index slipped 0.7 points to 93.1 in May, “ https://apnews.com/article/confidence-inflation-economy-4f681cecfa63fe251f5bb12bb4b949c6 #inflation #economy #consumerconfidence

Updated May 26, 2026 9:05 AM

WASHINGTON (AP) — U.S. consumer confidence declined slightly this month as gas prices stayed high and inflation remained elevated, a sharp contrast to soaring stock prices hover near record levels. The Conference Board’s consumer confidence index slipped 0.7 points to 93.1 in May, “ https://apnews.com/article/confidence-inflation-economy-4f681cecfa63fe251f5bb12bb4b949c6 #inflation #economy #consumerconfidence

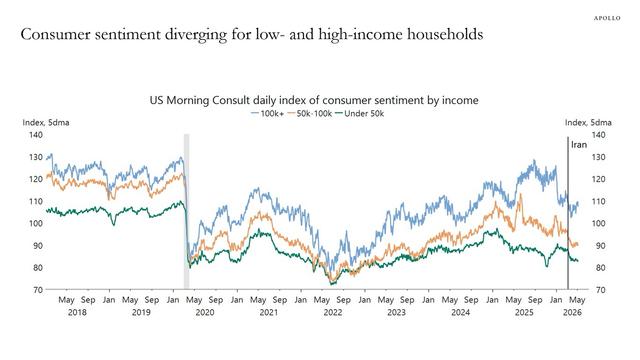

Most Americans are cutting back even as US markets roar, survey shows

U.S. consumer confidence declined slightly this month as gas prices stayed high and inflation remained elevated, a sharp contrast to soaring stock prices that have neared record levels. The Conference Board’s consumer confidence index on Tuesday slipped 0.7 points to 93.1 in May, the first decline after three months of gains. Americans have soured on President Trump’s economic policies, polls show, potentially creating problems for Republicans heading into the midterm elections. Gas prices have soared to a nationwide average of $4.49 a gallon from $2.98 just before the war began at the end of February, and have been at or above $4.50 a gallon for nearly all of May.