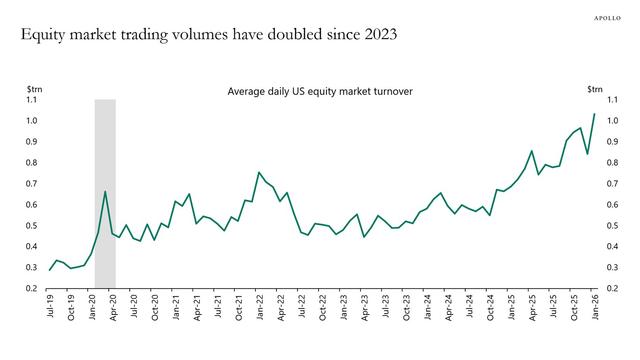

Dr. #TorstenSlok, Chief Economist, Apollo Global Management, The average daily #US #equitymarket turnover now exceeds $1 trillion, driven by higher #retail participation, more #high-frequencytrading and recent #tech-sector #volatility

🧵 (5/5) In trading, end-to-end latency from sensing the market to executing the action (new order single, amend, cancellation) determines whether the agent's reward signal is meaningful or just random noise.

Cross disciplinary research rocks. More later.

#ReinforcementLearning #AlgorithmicTrading #Latency #JohnCarmack #HighFrequencyTrading #Trading

Ultra-Low-Latency Trading System

https://submicro.krishnabajpai.me/

#HackerNews #UltraLowLatency #Trading #System #AlgorithmicTrading #FinTech #HighFrequencyTrading #StockMarket