A forecast of the fair market value of SpaceX's businesses

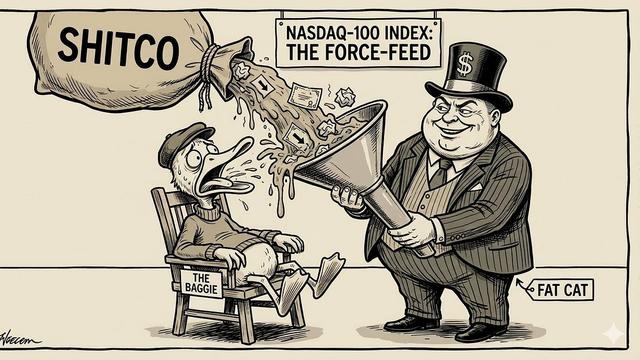

An passive investors are going to get hosed by this thanks to NASDAQ cooking the rules to favor Elon and his band of misfits.

No longer will there be a year of price discovery for index funds, 15 days. Meaning index funds have to buy it at the peak of the hype cycle. Will be a huge wealth transfer from mom and pop retirement accounts to the ultra wealthy.

Now I need a fund that will honor a year of price discovery rather than 15 days. Any recommendations?

Legally, any fund that tracks the NASDAQ 100 must follow the rules set by NASDAQ, so you'd want something that is neither a total market index, nor tracks the NASDAQ. Something like an S&P500 index would work

What law prevents someone from choosing to buy stocks from the NASDAQ 100 however they want for a fund?

You can make a mutual fund or ETF with any stocks you want, you just can't call it a NASDAQ 100 fund if you're not tracking the NASDAQ 100 index.

Is that really true? It doesn’t sound likely to me. Then again I’m often surprised by this stuff.

In order to call it a NASDAQ 100 Tracking Fund you need to pay the NASDAQ a licensing fee (same with S&P500, Wilshire 5000, etc.). The contract you have with NASDAQ will determine exactly how much freedom you have to change rules and still call it a NASDAQ 100 fund. I've never seen a licensing agreement, don't know anything about how they would typically read.

There is also the concept of "Index Tracking Error". No fund can perfectly mimic the index, and that is expected and understood, but the goal is generally to have the tracking error <0.1%- 1% would be a bad track. And so an index fund could take the risk that they will have a tracking error and delay picking up SpaceX even after it joins the official index, but then if it goes up they will look worse relative to their real competitors, the other NASDAQ 100 tracking index funds. If SpaceX goes down, of course, they will have positive tracking error, but I'm not sure how much potential investors would value that. SpaceX would be something like 4% of the NASDAQ 100 at it's announced expected market cap, so a 10% movement by SpaceX would be enough on its own to get you into the notable tracking error range if you didn't have any exposure to it.

It's an interesting question whether you could legally track the NASDAQ 100 without calling it that, or something very similar, e.g. "NASDAQ 100, but with a one year delay for new listings".

But assuming it is: How would you even call it, and how would you describe your methodology in the prospectus? "Tech 100 (compare with e.g. NASDAQ)"?

Actively managed funds like that charge around 0.5% to 1% a year. E.g. [0] The most prominent Nasdaq ETF, QQQ, charges 0.2% [1]

Spacex will be around 4.5% of the index [2].

If you believe the thesis of the article that Spacex is about 30% overvalued, and if the only advantage your fund manager has over the rest of the market is that they will avoid Spacex, they will save you 1% of your money over the lifetime of your investment. Assuming you're saving for retirement in 30 years time, the fees will cost you 15% or more.

Maybe your fund manager finds a Spacex-level mispricing every two years. In that case, they're worth the fees. Some people will tell you nobody can beat the market. My employer among others believes very strongly in the idea that some people do make better investment decisions than average. What is certainly true is that not everyone does.

[0] https://helpcenter.ark-funds.com/what-is-the-fee-structure-e...

[1] https://www.invesco.com/qqq-etf/en/home.html

[2] https://www.fool.com/investing/2026/04/01/how-the-spacex-cou...

> the idea that some people do make better investment decisions than average.

Of course some do. After all, that's what makes an "average".

Some people are taller than average, too!

They mean consistently make better decisions than a baseline index investor in a way that isn't luck.

Someone can win at roulette and make more money than the average player over some measurement period, but nobody can be good at roulette (when properly implemented and stuff). Stocks are somewhat possible to be good at but results are mostly random and the fee you'd pay is usually way too much.

>that isn't float adjusted?

AFAIK the problem is that they're lobbying the nasdaq 100 index provider to add a 5x multiplier for free float for spacex. Otherwise it would be far less controversial.

> Legally, any fund that tracks the NASDAQ 100 must follow the rules set by NASDAQ

No? Contractually, maybe. But legally you can do whatever you want with index constructions.

> An passive investors are going to get hosed by this thanks to NASDAQ cooking the rules

I’m genuinely confused how a passive investor winds up tracking the NASDAQ 100 versus a broader index.

Also, if you’re picking and choosing your exposures, you aren’t passive.

When index funds became such a default I knew they’d change the rules.

They’re taking everything thats not nailed down. A wealth tax is the only way, it cannot continue like this.

Yeah imma get out of index and hold my basket and just rebalance. This is dumb. Why bend the rules for a trillionaire?

> Why bend the rules[?]

> for a trillionaire[!]

This writes itself. It shouldn't, but "should" as a concept needs a lot of work.

And even that isn't accurate. They are not bending the rules for a trillionaire, they are maintaining the consistency more systemic rules. This is how it has always been. We can all point to real or perceived ethical islands. They certainly exist, and are worth creating and preserving. But for now, the sea still sets the rules, and the sea is deep. For the deeper system, island visibility is a useful distraction. Sometimes something heavy moves near the surface and we misinterpret visibility as exception.

Did you get lost and start writing a poem? What’s all this about the “sea”? Fine. Let me turn down my anti-Elon-ness for a bit and caveat that the timing of these changes coinciding with this listing is suspicious, no? Grant me that at least. And then we can, with new found common ground, investigate the motives behind such a change.

Someone who can't articulate who the villains are out of a pre-selected list and has to fall back to personal attacks is pretty "weak" as well.

If you were to apply the principle of charity[0] to the person you originally asked the question to, who do you think that they would mean by the word 'they' in this context?

Open your eyes? Everyone on the top 1000 Forbes and at trumps inauguration?

The unknown subject is a valid construction in language. It is not necessary to be able to answer "who's they?". It is semantically equivalent to saying "I knew the rules would be changed."

There are also perfectly ordinary situations in which this pattern is used to imply the influence of an unknown party. "They built a bridge over the river." Clearly the speaker does not believe that bridges over rivers construct themselves. She doesn't need to know who built the bridge.

>There are also perfectly ordinary situations in which this construction is used to infer the influence of an unknown party. "They built a bridge over the river." Clearly the speaker does not believe that bridges over rivers construct themselves. She doesn't need to know who built the bridge.

This excuse only works if who built the bridge isn't central to the discussion. Otherwise this is just generic conspiratorial thinking that we're being oppressed by The Elites™.

Aren't we, though? Like it's hard not to argue that there's one or more groups of people that get together at lunches and dinners and galas and have ongoing projects to do things like institute rule changes at NASDAQ that effectively require index funds to take on outsize risk from a known-overvalued IPO just in time for that IPO to happen.

To understand why this isn't a conspiracy of a sort by some "elite" group of people to take money from 401ks and IRAs, you'd have to argue that there's a good reason to shorten the window that outweighs the reason the window exists. The fact remains that many many IPOs crater within a few months. The rule change seems to exist to leave small low-effort investors holding the bag.

Just because we're paranoid doesn't mean they're not out to get us.

>Like it's hard not to argue that there's one or more groups of people that get together at lunches and dinners and galas and have ongoing projects to do things like institute rule changes at NASDAQ that effectively require index funds to take on outsize risk from a known-overvalued IPO just in time for that IPO to happen.

It's also not hard to think of half a dozen other groups that could possibly benefit and plausibly have enough clout to steer things in their favor, hence why the need to make a specific claim rather than beating around the bush a vague "they" that can't be refuted.

Got a source on this? I didn't take into account in this forecast that public markets could be very inefficient in this way.

oh baby, that's the just 'new' way they screw ya

Wow! This comment inspired me to dig deeper.

After 20+ years in the market, today I learned: "The S&P 500 is a float-adjusted, market-capitalization-weighted index."

So presumably an S&P 500 index fund is not disadvantaged, since it is tracking a float-adjusted index, i.e. the weight of SpaceX will be tiny if its float is tiny.

Or, is there a nuance that I'm missing?

>So presumably an S&P 500 index fund is not disadvantaged, since it is tracking a float-adjusted index, i.e. the weight of SpaceX will be tiny if its float is tiny.

Nasdaq already caved. FTSE and S&P are supposedly considering it.

https://www.economist.com/leaders/2026/03/31/index-providers...

Low float, large cap companies will get a 5x multiplier.

Huh, TIL, thank you.

Seems like MSCI can add new large constituents very quickly as well [1], so to remain neutral to the frenzy until a price has been discovered, one might need to actively short.

[1] e.g. https://www.msci.com/eqb/methodology/meth_docs/MSCI_GIMIMeth...