📣📣📣 REMINDER: The 2023 #ACA Open Enrollment Period is currently underway!

Here's 1️⃣3️⃣ important things to remember before. you #GetCovered: https://acasignups.net/22/11/02/its-time-again-heres-13-important-things-remember-you-getcovered-2023 #Healthcare #HealthInsurance #Obamacare #OpenEnrollment

It's That Time Again! Here's 13 important things to remember before you #GetCovered for 2023!

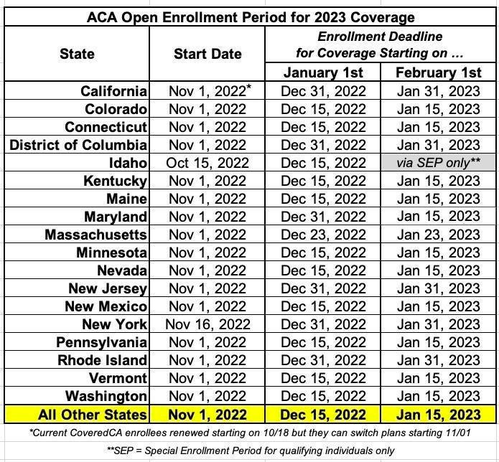

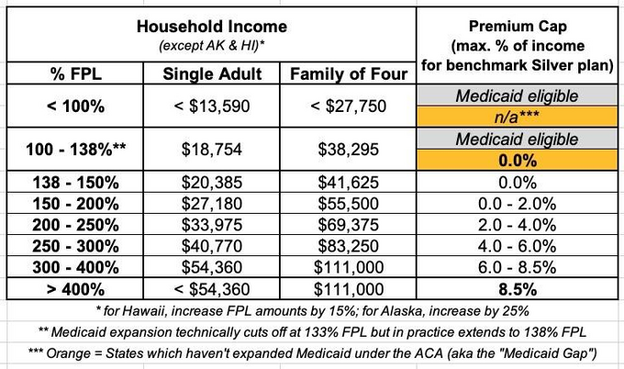

Tuesday, November 1st is the start of the official 2023 #ACA Open Enrollment Period (OEP) for anyone who needs quality, affordable healthcare coverage. The 2023 OEP is the best ever for the ACA for several reasons: First, the expanded/enhanced premium subsidies first introduced in 2021 via the American Rescue Plan, which make premiums more affordable for those who already qualified while expanding eligibility to millions who weren't previously eligible, are continuing for at least another 3 years via the Inflation Reduction Act; Second, because several states are either expanding or retooling their own state-based subsidy programs to make ACA plans even more affordable for their enrollees; And third, because millions more Americans who weren't previously eligible for ACA subsidies (even with the expanded ARP/IRA enhancements) are now eligible via the Biden Administration's closure of the so-called "Family Glitch." There's also expanded carrier & plan offerings in many states/counties, and as always, millions of people will be eligible for zero premium comprehensive major medical policies. If you've never enrolled in an ACA healthcare policy before, or if you looked into it a few years back but weren't impressed, please give it another shot now.