Thanks to @[email protected] for properly quoting and citing me in his new story.

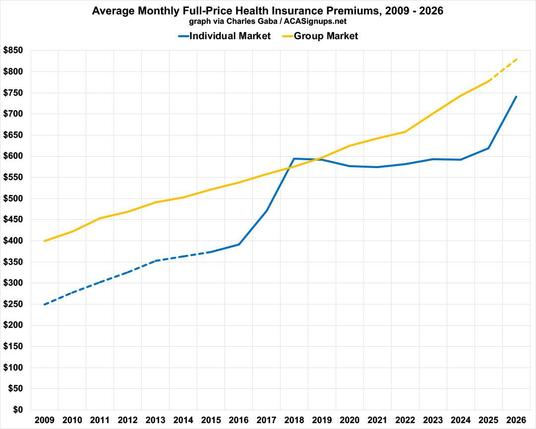

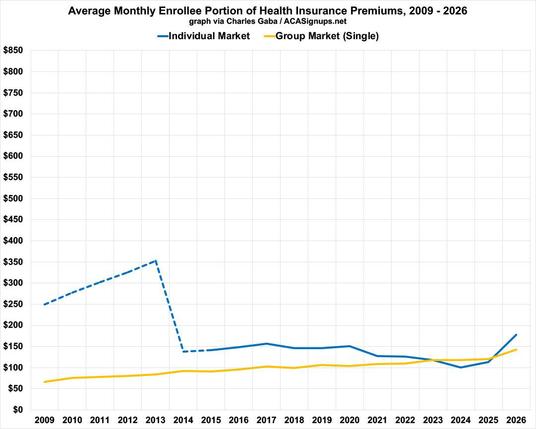

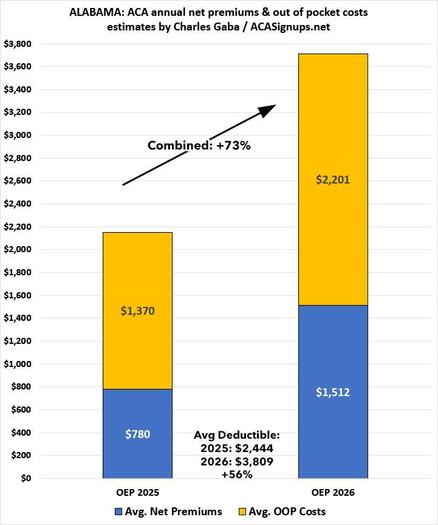

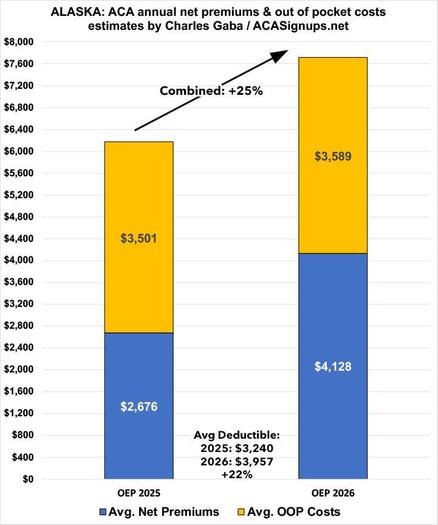

FWIW, our conversation was the inspiration for this post of mine which compares increases in individual market premiums vs. employer-sponsored insurance:

charlesgaba.substack.com/p/which-cost...

RE: https://bsky.app/profile/did:plc:o6lyhdte6gtwvkcdnrhm5doj/post/3mmtjdjsfoc2j

Which costs more: Employer-Bas...

RE: https://bsky.app/profile/did:plc:o6lyhdte6gtwvkcdnrhm5doj/post/3mmtjdjsfoc2j

Which costs more: Employer-Bas...