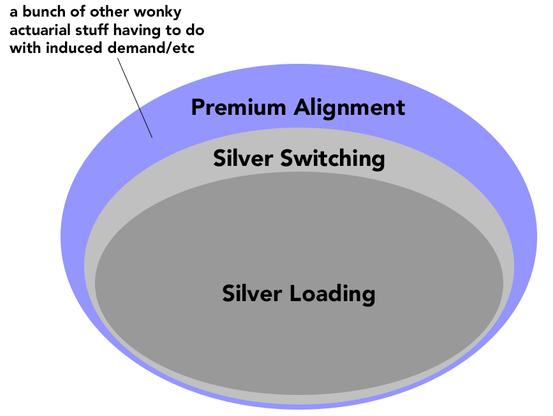

HEY TEXAS ACA ENROLLEES: Here's an article about #SilverLoading & #PremiumAlignment which puts them in pretty easy-to-understand terms:

www.houstonchronicle.com/politics/tex...

Why a little-known state law m...

Why a little-known state law m...

As anyone not under a rock for the past few months knows by now, the improved federal Affordable Care Act tax credits which were put into place by President Biden and Congressional Democrats starting in 2021 are currently scheduled to expire at the end of December, just 2 1/2 months from now. If this happens, the consequences for ~24 million Americans will be devastating, with average health insurance premiums more than doubling and millions being priced completely out of the insurance market altogether. On top of this, the Trump Regime has also made administrative regulatory changes to how the ACA is structured resulting in the remaining tax credit formula becoming even less generous yet, while also eliminating eligibility for either financial assistance or even ACA enrollment whatsoever to many other Americans. Congressional Republicans could still potentially agree to extend the tax credit upgrade, but that's extremely unlikely at this point, and even if they do, some of the other executive actions taken by the Centers for Medicare & Medicaid Services (CMS) under Trump, RFK Jr. and Dr. Oz would still negatively impact a lot of people.