Necessity is the mother of invention

Necessity is the mother of invention

I’ll do one better:

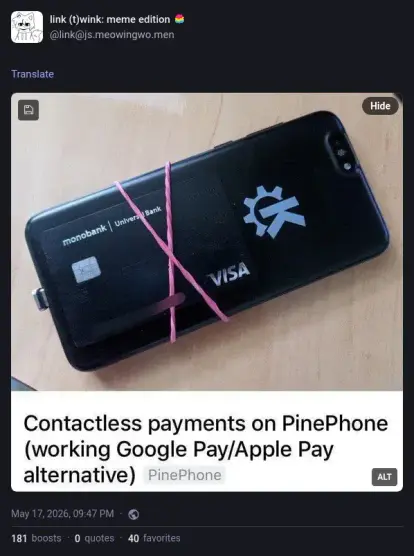

My payment card was just a bit too wide to fit in my cellphone’s cover. The phone’s own NFC antenna is at the top - and I use it all the time - so the card had to be at the bottom of the cover to avoid triggering the phone all the time, in portrait orientation so-to-speak.

So I dissolved the card in acetone to extract the NFC chip and its antenna, then carefully reshaped one end of the antenna so it’s a bit less wide (and since I couldn’t modify the length of the wire or the number of turns in any way to avoid de-tuning the antenna too much, I sort of accordioned one side of the rectangle to accommodate the extra wire).

Then I set the new shape of the antenna permanently by carefully applying a piece of packing tape over it, flipped it over, taped over the other side to seal everything, then carefully cut around the new, ultra-thin, stubbier contactless payment “card”.

Now it fits really smartly in my cellphone cover!

I was thinking about this, and there are two easy workarounds, I think:

But, in either case, I do think you might run into a different issue: automated fraud detection sometimes requires me to chip+PIN, even for transcribed below the tap limit. This has happened to me when traveling. I don’t think there would be any way around that, and if you then fail to authenticate with chip+PIN, it’s reasonable to think that the bank would lock your card for contactless payments until you successfully authenticate the card again with chip+PIN. (To be clear: this is only speculation; not sure if that would be an issue in practice.)

So, I suspect that whether this would work or not might depend on your institution (or maybe jurisdiction?)