I think some people are getting really confused about what it means when there is inflation and real wage declines. Textbook models of wage and price Phillips curve tells us that if price growth>nominal wage growth, it's unlikely from labor market tightness.

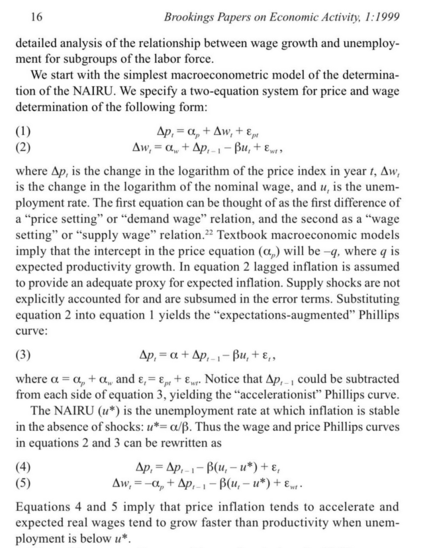

This comes right off the 1999 analysis by @lkatz42 and Krueger in their BPEA. Take the difference between equations 4 and 5: that's the real wage growth. Tightness will raise nominal wage and price similarly. If price growth > nominal wage growth, gap likely from supply shocks.

This is where having simple formal models can help clarify logic of arguments and avoid talking in circles. Doesn't mean the model is right. Just disciplines conversations and arguments.

Cc @paulkrugman @Noahpinion

To be clear, I'm NOT saying that tightness in the labor market has no impact on inflation today. It very well might (more on this later).

What I AM saying is that it can't be the primary factor according to textbook models when price growth>>average nominal wage growth.

We've run *a lot* of regional panel wage and Phillips curves of late! I'm not going to tweet out results until our paper is out. But suffice it to say that (properly defined) tightness predicts nominal wage and price growth not very different from the simple model I linked above.