The SpaceX IPO: retail investor notes

https://report.bearblog.dev/the-spacex-ipo-will-be-the-perfect-storm-of-retail-investor-fallacies/

The SpaceX IPO: retail investor notes

https://report.bearblog.dev/the-spacex-ipo-will-be-the-perfect-storm-of-retail-investor-fallacies/

These two comments seem to tell you, everything you need to know about this IPO. Sadly I cant get the same level of analysis, from CNBC or Bloomberg, so have to come here...

The bigger investors know the dual-use story for SpaceX, so that is what will be used to justify valuations.

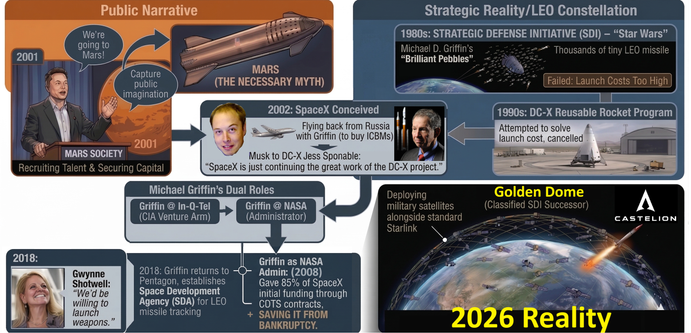

Attached: 1 image SpaceX lacks the hardware or a plan with scientific viability for a genuine Mars program. The scientific community has long recognized the facade. A feasibility study published in the journal Nature definitively concluded that a crewed Mars mission using Starship is unworkable. The vehicle’s massive dry weight creates a severe Delta-v deficit, making a return flight physically impossible. Furthermore, the architecture lacks closed-loop life support and relies on massive, non-existent nuclear power and water-mining infrastructure. Instead of building for Mars, Starship is a heavy-lift vehicle with low characteristic energy (C3). This is only a reasonable design for driving mass to low-Earth-orbit constellations—a trajectory that perfectly mirrors decades-old Pentagon objectives, that recently has manifested as Golden Dome. In the 1980s, Michael D. Griffin architected "Brilliant Pebbles," a global missile-interceptor network made up of thousands of weaponized satellites in Low Earth Orbit. It died alongside Reagan's Strategic Defense Initiative in 1990s after the DC-X reusable rocket program failed to lower launch costs. The architectural dream survived through "New Space" advocacy. Griffin co-founded the Mars Society and recruited Elon Musk after he was brought to his attention by Peter Thiel. In 2001 Griffin and the young Musk traveled together to Russia to examine ICBMs. SpaceX was conceived on the flight home to solve the exact launch bottleneck that killed Brilliant Pebbles. Musk later admitted the company was simply "continuing the great work of the DC-X project," and it was ultimately Griffin—later acting as NASA Administrator—who awarded billions of dollars in contracts that saved a zero-experience SpaceX from bankruptcy. SpaceX masking began to slip when Gwynne Shotwell publicly confirmed the company's willingness to launch offensive weapons in 2018. That same year, Griffin returned to the Pentagon to establish the Space Development Agency, mandated to build a proliferated LEO constellation for hypersonic missile tracking. In 2019, U.S. General Terrence O'Shaughnessy pitched the Senate on "SHIELD"-a layered orbital missile defense system. Shortly after, O'Shaughnessy retired from the military and joined SpaceX to lead their discreet new division: Starshield. Three decades later, Brilliant Pebbles is finally materializing as Golden Dome. As Reuters reported, Musk's Starshield is the frontrunner to build this classified SDI successor, pitching the Pentagon on a Golden Dome architecture involving thousands of weapon satellites. Starshield is already deploying these military satellites alongside standard Starlink satellites. Mars was the necessary myth to recruit talent, capture public imagination, and secure capital. But as the Nature study proves, Starship was never physically capable of planetary colonization. The capabilities SpaceX actually delivered...cheap mass-to-orbit and rapid satellite replenishment...are the exact prerequisites of Golden Dome. https://en.wikipedia.org/wiki/Golden_Dome_(missile_defense_system)

This other comment by the same user in one of the links from 2 weeks ago I found the easiest to understand, in brief:

If S&P change their rules, I am going to sell my index funds, taxes be damned.

Sadly, this is not the only trash that is going to be hoisted on us retirement investors. OpenAI is waiting in the wings as well.

I am sure I am not the only one. That doesn't seem like it will be good for the market.

There were extensive discussions previously about passive investors being taken for a ride:

https://news.ycombinator.com/item?id=47392550

And Michael Burry also wrote a long post about it:

https://x.com/michaeljburry/status/2032483200404992209

The question is what can we do about it? Nasdaq finalized these rule changes already. It seems like this got rammed through and now it is happening. And I don't expect Trump's corrupt SEC to do anything about it. Who else can we appeal to?

> Unfortunately, shorting it means betting that space data centers won’t happen (I’d happily take that bet)

This seems like an easy bet to win, though I don't know what you were responding to now that it's flagged. It's hard to imagine 'space data centers' being a meaningful product or infra in the collective lifetimes of anyone posting on this site.

> Two-Stage Discounted Cash Flow (DCF) model. It is the gold standard for valuing a high-growth company like SpaceX.

I don't know if it's true that DCF is the "gold standard" for valuing high growth companies. IME it's actually quite bad -- not that there's really good ways to value them; more that DCF is much better for companies that aren't high growth.

High growth companies - especially ones run by Musk -- are intrinsically very hard to value, for reasons like:

- They sometimes - unpredictably - spawn new categories (think Starlink)

- There are too many variables to be able to reliably predict future cash flows (compared to say, an oil company, where future cash flows are largely dependent on oil prices, which can also be forecast with some degree of certainty)

- Risk has a much higher impact on a high growth company, how does DCF try to quantify that? Sure, you can ramp up your risk free rate like TFA suggests, but that's about as coarse a measure as it gets. Consider the risks to e.g. Tesla, how do you quantify them and their impact on its future cash flows?

Actually all this can be captured in DCF, which incorporates continuous risks with the assumption of being a going concern.

What it does not incorporate is failure risk, which has to be brought in separately.

Pricing via relative valuation is implicitly DCF… so you can’t escape it actually. If you want to do some pie in the sky shit and pull a number out of thin air - go ahead.