Your periodic reminder that bailing out Silicon Valley Bank cost more than the entire US food stamp program, and happened overnight with zero debate.

@tprophet but the bank wasnt bailed out, no?

@clsytim @tprophet if you want to break down each word like a lawyer, no. If you want to describe the action of covering and restoring uninsured funds that were lost, then yes.

It's impossible to deny that a very large (to me) amount of money was conjured out of thin air, which is very surprising as we are always told that it would be an irresponsible amount of money to conjure up when normal people need it

@clsytim @tprophet @ATLeagle I don’t think we know the full breakdown yet.

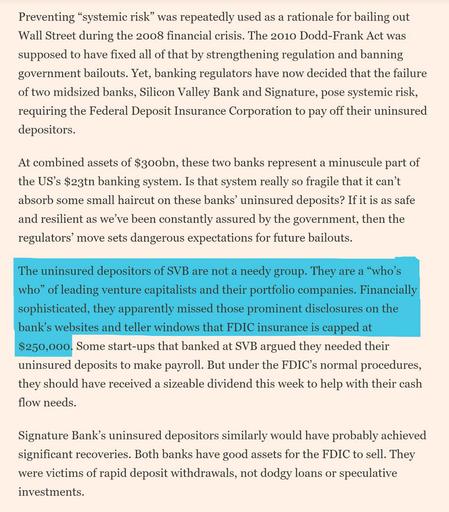

"At the end of 2022, the FDIC reported that its deposit insurance fund had a balance of $128bn, or about 1.27% of the total insured deposits, and far less than may be needed.”

…

"Funding for the non-bailout bailout will also come from selling off SVB and Signature assets, pegged at $212bn and $110bn respectively. "

….

"make no mistake – it does have an expected cost to taxpayers.”

https://www.theguardian.com/business/2023/mar/13/silicon-valley-bank-collapse-biden-bailout-question

@peterbutler @clsytim @tprophet @ATLeagle wow sounds like those banks might have failed to do a simple routine hedge.

Why is there no public banking option when we keep bailing them out and they're necessary? Why don't they get nationalized instead of bailed out when they fail?

@cykonot @peterbutler @clsytim @tprophet @ATLeagle they were nationalized. Fdic seizes the bank and then tries to sell it

@vy @peterbutler @clsytim @tprophet @ATLeagle selling off all the assets of a failed company is not the same as nationalizing it

@cykonot @peterbutler @clsytim @tprophet @ATLeagle It's currently under management of the FDIC and was taken from the bank shareholders.

@vy @peterbutler @clsytim @tprophet @ATLeagle ya it's being sold off not nationalized. There isn't a public bank run by the us federal government for people to use.

Breaking up a failed company and selling off the assets to others in the industry (many of whom you bailed out before) does not give us a public banking option. Why are you pretending it does

@cykonot @peterbutler @clsytim @tprophet @ATLeagle Did I say it gives us a public bank option? No. I just pointed out that SVB successor company, a totally government/FDIC owned company is operating the bank and its shareholders were zeroed out. I think we need a real Postal bank or public bank, but SVB was not bailed out, it was taken over by the government. Call it what you want.

@vy @peterbutler @clsytim @tprophet @ATLeagle depositors were bailed out. The former head of the FDIC literally called it a bail out.

The government winding down a company and selling off the assets to private industry (letting the private banks profit) IS NOT NATIONALIZATION. Words have meanings.

If California shut down PG&E and sold its assets to random companies they would not have nationalized their energy infrastructure. They would have just sold off a bunch of discounted assets

@cykonot @peterbutler @clsytim @tprophet @ATLeagle I really don't like "bailout" here because, as we've seen in this discussion, people think that the owners of SVB were paid.

@cykonot @peterbutler @clsytim @tprophet @ATLeagle i don’t particularly like that the vcs got no haircut and biggest corporate customers same but i imagine that within federal law and time limits it would have been hard for fdic to make funds rapidly available to everyone but the vc account holders

@vy @peterbutler @clsytim @tprophet @ATLeagle only the big boys were uninsured and they'd be mostly covered anyway

So not difficult. They just wanted to give their donors money

@cykonot @peterbutler @clsytim @tprophet @ATLeagle If they'd be mostly covered anyway, what are you complaining about?

@vy They shouldn't be getting public funds outside the insurance they paid for.

we can technically afford to indulge those awful fascists without further austerity, but those same people are still gonna push for austerity. so fuck them.

edit: are you advocating for the devil or sumn? whats with that question

@cykonot What makes you think they are getting public funds outside of the insurance? I don't see any evidence of that.

I can see why the admin didn't want to allow Thiel to spark a recession so that the nazis could win the next election, but I don't get what's in it for you? Seems like people are being resentful rather than strategic.

@vy that's what makes it a bailout. Why are you shilling

Edit: even if they just stole funds and forced rates to go up, the burdens of our system rest on the little guy. The higher rates will be used to justify taking away Medicaid or something lol

You wanna backstop private risk with public money bro? That sounds ineff6and immoral

@cykonot You didn't answer my question? What evidence do you have that they are getting money not from FDIC insurance?

And if you are going to make accusations of shilling, I got to ask why you are shilling for Theil?

@vy I obviated the argument by pointing out what would happen to the deposit insurance, dickhead

@vy @cykonot @peterbutler @clsytim @ATLeagle They absolutely could have made $250k immediately available, and Treasuries are liquid. It wouldn't exactly take a lot of time to sell them and hand everyone their 15% loss.

@cykonot @peterbutler @clsytim @tprophet @ATLeagle SVB succesor bank is operating. Who owns it? It will probably be sold, but it has not been yet and I don't think it should be.

@cykonot @peterbutler @clsytim @tprophet @ATLeagle the CEO of Silicon Valley Bank is responsible for its collapse.

@peterbutler @clsytim @tprophet @ATLeagle

"... a balance of $128bn, or about 1.27% of the total insured deposits.”

That's 1.27% of the ~entire US~ insured deposits. 1% isn't an unreasonably sized risk pool.

"As of Dec 31, 2022, #SVB had approximately $209.0bn in total assets and about $175.4bn in total deposits."

Subtract the $42bn withdrawn in the bank run and that's 209bn in assets to cover 133bn in deposits. Even if assets sold at 1/2 price, that's just 28bn out of the 128bn FDIC fund.

@exador23 @peterbutler @clsytim @ATLeagle Asset valuations aren't marked to market which was literally the whole root cause of this issue.

@tprophet @peterbutler @clsytim @ATLeagle

understood. which is why I calculated the cost of covering uninsured deposits based on a 50% loss on the assets. I seriously doubt the haircut will be that bad, though.

@tprophet @peterbutler @clsytim @ATLeagle

We have official estimates from the chair of the FDIC now:

“The FDIC estimates that the cost to the DIF [Deposit Insurance Fund] of resolving SVB [Silicon Valley Bank] to be $20 billion. The FDIC estimates the cost of resolving Signature Bank to be $2.5 billion. Of the estimated loss amounts, approximately 88 percent, or $18 billion, is attributable to the cost of covering uninsured deposits at SVB…”

@exador23 @peterbutler @clsytim @ATLeagle Oh, ok, so it ended up being the entirety of what the US spends addressing climate change (which was a subject of approximately zero debate, right?) https://www.whitehouse.gov/wp-content/uploads/2022/03/budget_fy2023.pdf

@exador23 @tprophet @clsytim @ATLeagle The FDIC claims there will be a “special assessment” to force big banks to help pay for it

FDIC Considers Forcing Big Banks to Pay Up After $23 Billion Hit

The Federal Deposit Insurance Corp., facing almost $23 billion in costs from recent bank failures, is considering steering a larger-than-usual portion of that burden to the nation’s biggest banks, according to people with knowledge of the matter.

@peterbutler @exador23 @clsytim @ATLeagle Yes, they'll raise their fees and pay less interest to pay for it. You don't think that's coming out of shareholder returns and executive bonuses, do you?

@tprophet @peterbutler @exador23 @clsytim yep. There were promises made that some small banks may get exceptions to the new increased charge to cover this. So friends and well connected people get breaks. Will this stress small banks? Probably. Will it end as an advantage to big banks? Definitely

And it's precedent that the rules aren't actually rules.

@peterbutler @tprophet @exador23 @clsytim I've been in local credit unions for a very long time. Ever since bank of America kept buying every small local bank who actually tried to care about customers. It became impossible to run from those jerks

@ATLeagle @peterbutler @exador23 @clsytim The rules would totally have been rules if the depositors were ordinary people rather than Silicon Valley billionaires.

@peterbutler @clsytim @tprophet @ATLeagle So, the best number I can find for food stamps is $113.74 billion for 1969 to 2021 (source: https://www.statista.com/statistics/315032/us-supplemental-nutrition-assistance-program-total-costs/ )

According to FDIC, SVB had $175.4 billion in deposits, and assets with a book value of $209 billion ( https://www.fdic.gov/news/press-releases/2023/pr23016.html ).

While we can expect the sale value of SVBs assets to fall below the book value, they'd need to fall a fair way for TProphets statement to be true, unless we're including other non-SVB related costs in the calculation.

@clsytim @tprophet I see it as I have insured my home to a certain amount. If I actually needed 10x that, then even if my insurance company had assets that COULD cover me, they wouldn't, because I hadn't actually insured correctly. These companies could have done this, chose not to, yet were made whole.

The same people yelling that everyone else needs to own their mistakes and be responsible are supporting these recovery funds.

@clsytim I heard news stories saying it was all from the fund, but that bank assessments may rise as a result.