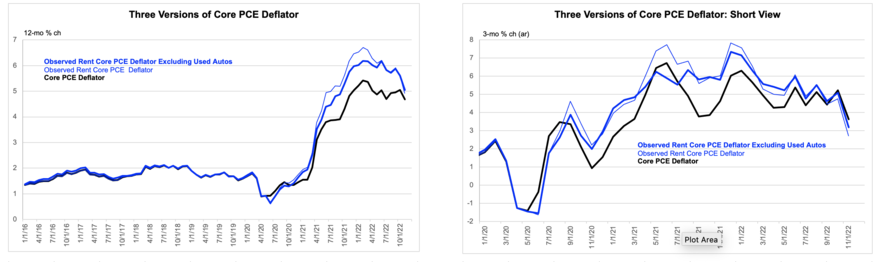

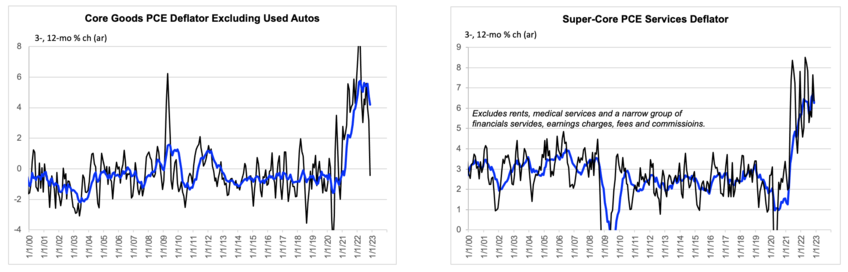

This has been driven by developments in two sectors: the goods sector, even net of used cars, and housing as marginal rents, whose whose inflation rate has apparently fallen to near zero. But the peak disinflationary force from those two sectors is probably now in the data, at least on my metrics. (Official rent data are separate.) So until the labor market cools off, further disinflation from here, i.e. into a range acceptable to the Fed, seems not the base case.