I did not expect that from the BOJ today, but it makes some sense.

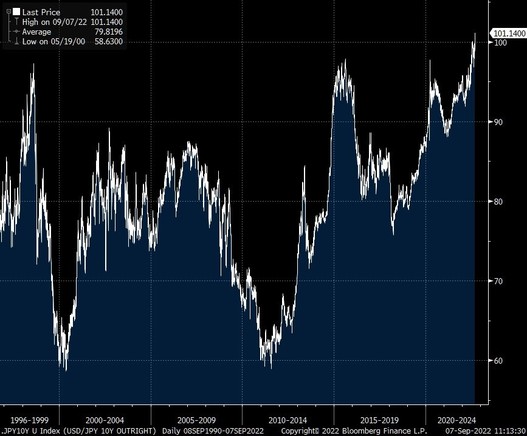

30y was at 1.40+. 15yr at 0.83, and a straight line from 5 to 15 would pass through 10y at 50.

Someone will make bank on the jump in 10yr yields today. Some will decide to be short the follow because of good trade skew.

This move steepens the front and makes bank lending easier (because when there is a kink in the curve, things get a trifle wonky with customers).

[repost from The Other Place]